x

Silver prices remained stable on Tuesday, hovering just above $33.00 an ounce and staying within the prior week’s trading range. This steadiness mirrored gold’s marginal decline after recent volatility, as the precious metals markets calmed following gold’s peak of over $3,500 an ounce on April 22. Easing tensions between the US and China, particularly regarding tariff disputes, provided some relief to financial markets, although underlying macroeconomic risks tied to US trade policies persist.

The gold-to-silver ratio has widened significantly, rising above 100 — a sharp increase from the typical 80–90 range seen over the past three years. This shift highlights gold’s stronger appeal as a safe haven amid economic uncertainty, in contrast to silver’s vulnerability to reduced industrial demand in a slowing global economy. Market participants are now focused on key economic data releases this week, including Q1 GDP figures for both the Euro Area and US, the US core PCE index, and employment data. These indicators will likely influence expectations for US interest rate policy, with traders currently pricing in a significant chance of a rate cut at the Federal Reserve’s June meeting. Source

Gold prices edged slightly lower on Tuesday, trading within a narrower range of $3,300 to $3,342 an ounce compared to the previous day, as markets digested signs of a possible easing in the US-led trade tensions that had unsettled investors in recent weeks. Since reaching an all-time high of over $3,500 an ounce on April 22, gold has mostly traded sideways near $3,300, with its rally stalling amid speculation that President Trump may need to soften his trade tariff stance to avoid political and economic fallout.

Despite the lack of upward momentum, gold’s resilience near current levels suggests that markets remain cautious due to lingering uncertainty over US trade policies and their global economic repercussions. This caution has weakened higher-risk assets like equities, while maintaining demand for safe-haven assets such as gold. Technically, gold is stable below minor resistance at $3,371, with key support around $3,170 if downward pressure returns. Traders are now focused on upcoming economic data — notably Q1 GDP figures for the Euro Area and US, and the US core PCE index — which could shape expectations around future interest rate movements. Source

The World Bank has revised its outlook, forecasting that gold will outperform silver through 2025 and beyond, buoyed by persistent safe-haven demand amid geopolitical tensions, market volatility, and global uncertainty. Despite gold's recent surge to an all-time high of $3,500 an ounce, analysts expect no major correction, with average prices projected at $3,250 an ounce in 2025 and $3,200 in 2026—both well above historical averages. The bank emphasized that if geopolitical tensions intensify further, gold prices could surpass even these optimistic forecasts, cementing its position as the standout asset in the commodity space over the next two years.

In contrast, while silver is still expected to perform strongly, the World Bank has scaled back its previous expectation that it would outpace gold. Silver prices are forecast to average $33 an ounce this year and rise modestly to $34 an ounce by 2026, supported by robust industrial demand, particularly from sectors like renewable energy and semiconductors. However, economic slowdowns and recent tariff announcements pose risks to these industries. Both gold and silver are anticipated to outperform the broader commodity market, which is expected to decline due to weaker economic growth and falling oil prices. The World Bank noted that a turnaround in commodity prices hinges on improved global economic prospects and a rollback of trade restrictions. Source

Harry Mamaysky, professor at Columbia Business School and partner at QuantStreet Capital, argues that after a stellar 42% rise in gold prices over the past year, it’s worth reassessing the case for holding gold. In his analysis, he highlights gold’s strong performance relative to other major asset classes, driven largely by economic uncertainty and recent trade tensions under the Trump administration. Key supportive factors include consistent central bank buying, gold’s low correlation with other assets (making it an effective portfolio diversifier), and its resilience during weak equity markets. Mamaysky also notes that QuantStreet’s machine learning model remains bullish on gold, pointing to factors like the U.S.–Germany interest rate differential and elevated U.S. two-year Treasury yields as drivers of strong forward-looking returns.

However, Mamaysky cautions that gold’s historically high valuation relative to consumer prices suggests investors should proceed carefully. He points out that the gold-to-price-level ratio has reached an all-time high, signalling potential overvaluation risks. While other factors, such as the gold-to-bitcoin ratio and ongoing geopolitical uncertainty, continue to support gold as a hedge, Mamaysky emphasizes the importance of active portfolio management. QuantStreet still holds gold but is prepared to adjust its position as market conditions and relative opportunities evolve in the coming months. Source

Bernard Dahdah, commodity analyst at Natixis, argues that despite recent volatility and a pullback from gold’s all-time high of $3,500 an ounce, the metal still has significant upside potential, potentially reaching $4,000 an ounce. While easing U.S.–China trade tensions have reduced some immediate geopolitical risks, underlying uncertainties persist, keeping gold attractive as a safe-haven asset. Dahdah highlights that weakening confidence in U.S. dollar assets, particularly U.S. Treasuries and money market funds (MMFs), is benefiting gold. Recent data shows a sharp outflow from MMFs — the largest since the financial crisis — as investors question the reliability of traditional U.S. safe havens. This shift could drive sustained demand for gold, with Natixis forecasting an average price of $3,150 an ounce in 2025 and $3,360 in 2026.

On the downside, Dahdah notes that gold appears to be establishing a firm support level around $3,000 an ounce, which could strengthen further if China begins selling U.S. Treasuries or if MMF outflows persist. Chinese demand remains a crucial factor in gold pricing, as evidenced by the elevated Shanghai gold premium, which reflects strong appetite from Chinese buyers in response to tariff threats. Although the premium has eased from its peak, it remains well above historical averages, indicating sustained interest. Overall, while gold’s immediate price movements may be volatile, structural shifts in investor sentiment toward U.S. assets and robust Chinese demand provide a solid foundation for long-term strength. Source

Image Source: Kitco News

Gold futures have shown notable stability, consistently holding above the key $3,300 support level following their record high of $3,509.90 on April 22. Over five consecutive trading sessions, prices have oscillated within a narrowing range, with daily fluctuations averaging around $30. Despite the recent consolidation, gold’s resilience is underpinned by its ability to open and close within a tight band between $3,301 and $3,367, signalling strong underlying support even amid reduced market volatility.

This stability coincides with weakening U.S. economic indicators, including a record trade deficit, declining consumer expectations, falling job openings, and a sharp drop in consumer confidence. These signs of economic fragility, alongside upcoming key data releases — such as the PCE inflation index, Q1 GDP, and nonfarm payrolls — will be closely watched by both markets and the Federal Reserve. Although rate cut expectations remain low for May, persistent economic weakness and gold’s safe-haven appeal suggest potential for another upward move. If upcoming data further confirms slowing U.S. growth, gold prices could break out of their current consolidation and push toward new record highs. Source

Global gold demand surged to 1,206 tonnes in Q1 2025, marking its strongest start to a year since 2016, driven by rising economic uncertainty and geopolitical risks, according to the World Gold Council. Robust investor interest in physical bars, coins, and gold-backed ETFs, alongside steady central bank purchases, underpinned this growth. Investors, wary of frothy risk assets and increasingly skeptical of U.S. Treasuries amid global trade tensions, have turned to gold as a stable portfolio hedge. Notably, gold-backed ETFs saw a sharp reversal from outflows in 2024 to 226.5 tonnes of inflows this year, with Asian demand, particularly from China, surpassing North American levels. Despite gold’s record prices, investors appear less concerned with valuation and more focused on gold’s risk-mitigating qualities.

However, the market isn’t uniformly strong across all segments. Jewelry demand weakened sharply, falling 21% to 380.3 tonnes — the lowest level since the pandemic — as high gold prices deterred consumers, particularly in China where purchases dropped 35%. Despite this, industrial demand remained stable at 80.5 tonnes, suggesting underlying economic resilience. Central bank purchases slowed from last year’s record levels but remained above historical averages, and gold mine production hit a record Q1 high of 856 tonnes. With persistent uncertainty and strong fundamental buying, analysts anticipate continued robust support for gold prices going forward. Source

Gold prices faced selling pressure following ADP’s report showing only 62,000 jobs created in April, well below the expected 114,000, reflecting growing labor market weakness. Despite the decline, gold held above its session lows as weaker job growth and slowing wage inflation raised expectations that the Federal Reserve could cut interest rates, a move that would support gold as a safe-haven asset. Analysts noted that persistent economic uncertainty and softer labor data could bolster gold demand in the near term. Source

Gold prices faced continued profit-taking even as rising recession fears provided some limited support after U.S. GDP contracted by 0.3% in the first quarter of 2025—the first decline since 2022 and sharply weaker than the previous quarter's 2.4% growth. The contraction was driven by a rise in imports and lower government spending, partially offset by modest increases in investment, consumer spending, and exports. The report also revealed hotter-than-expected inflation, with the GDP Price Index climbing to 3.7%. Spot gold traded around $3,286 an ounce, down about 1% on the day, despite growing speculation that weak economic data could push the Federal Reserve toward interest rate cuts.

Analysts noted that while tariff threats from President Trump led to stockpiling and distorted trade data, underlying domestic and consumer activity showed signs of weakening. Consumer spending growth slowed to 1.8% from 4.0% in the prior quarter, adding to concerns about economic momentum. Some economists, however, downplayed immediate recession risks, suggesting that resolving trade tensions could restore stability. Still, the combination of the GDP report, weak labor market data, and deteriorating business sentiment signals increasing risks to the economic outlook in the months ahead, potentially enhancing gold's safe-haven appeal. Source

Gold prices were moderately lower in midday U.S. trading on Wednesday but rebounded from overnight lows after weaker-than-expected U.S. economic data, including a disappointing ADP employment report and a surprise contraction in first-quarter GDP. These figures strengthened the case for dovish monetary policy, potentially increasing pressure on the Federal Reserve to cut interest rates sooner. Despite the economic weakness, gold traded at $3,318.60, down $15.20, while silver saw a sharper decline to $32.605. Broader markets also reacted negatively, with U.S. stock indexes down and crude oil prices sharply lower, adding headwinds to precious metals. Meanwhile, China's economy showed signs of strain from escalating trade tensions with the U.S., as export orders fell to pandemic-era lows.

Technically, gold bulls still maintain a solid near-term advantage, with key resistance at $3,509.90 and support at $3,200.00. For silver, bulls also hold a near-term edge, with resistance at $35.00 and support at $32.00. Despite current profit-taking and external pressures, both metals remain in uptrends on daily charts, supported by safe-haven demand amid growing economic uncertainty. Key upcoming data, particularly Friday’s U.S. jobs report, could further shape market direction, influencing expectations for future Fed policy moves. Source

Silver prices have struggled below $33 an ounce, weighed down by global recession fears and reduced industrial consumption. However, analysts from BMO Capital Markets highlight that the solar power sector is a crucial factor that will keep the silver market in deficit for the foreseeable future. As global demand for renewable energy grows, silver remains a key component in photovoltaic solar panels. BMO estimates that the solar sector will consume 246 million ounces of silver in 2025, a 5.5% increase from the previous year, with demand peaking at 261 million ounces in 2026. The solar sector's growth has dramatically reshaped silver consumption, with usage increasing from just 54 million ounces a decade ago.

BMO analysts emphasize that despite challenges, the solar sector remains a bright spot in the global industrial economy, driven by the need for affordable, clean energy. Although China dominates the solar panel market and its costs have driven down the price of solar power, nations worldwide are likely to overlook trade protectionism to capitalize on the benefits of cheap energy. While silver usage per solar panel is expected to decrease slightly due to thrifting, this trend is nearing its limit, as silver remains essential for the efficiency of solar cells. As a result, BMO anticipates silver prices will remain in the $30 to $35 per ounce range, driven by sustained solar demand and limited supply growth. Source

Image Source: Kitco News

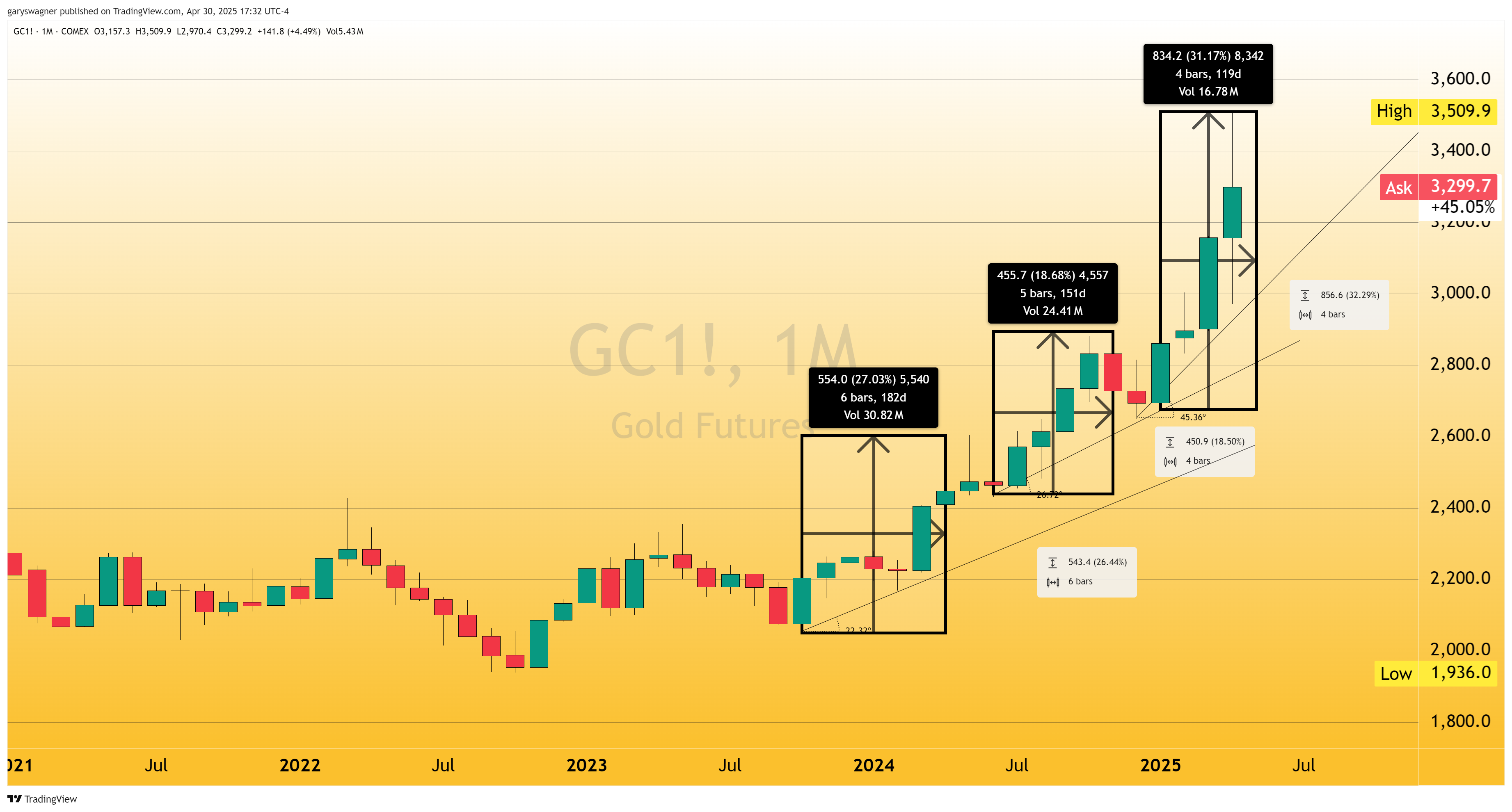

Gold has continued its impressive rally throughout 2025, achieving a remarkable 4.52% gain in April alone, pushing its value to $3,300.80 per ounce. This marks the fourth consecutive month of growth, building on a strong start to the year with gold appreciating by approximately 18% since January. The precious metal reached a historic high of $3,509.90 in April, driven by the weakening U.S. dollar, which has been significantly impacted by trade policies, including tariffs on imports. The declining value of the dollar has bolstered gold's appeal as a safe-haven asset, and despite some narrowing of its trading range toward the month's end, the fundamental factors supporting gold's price remain strong.

Gold's rally has been fueled by a combination of economic challenges both in the U.S. and globally. The U.S. economy contracted by 0.3% in the first quarter of 2025, falling short of growth expectations, while private sector job growth also slowed significantly. Additionally, China’s manufacturing sector showed signs of contraction, exacerbated by U.S. tariffs. These economic struggles, combined with geopolitical tensions, have reinforced gold’s role as a store of value. As uncertainty continues and the dollar remains weak, gold's upward trajectory seems likely to persist, even as it finds a more constrained trading range following its record highs. Source

Disclaimer: These articles are provided for informational purposes only. They are not offered or intended to be used as legal, tax, investment, financial, or any other advice.

Featured Image - Source: Unsplash