x

Gold and silver surged sharply as safe-haven buying intensified amid simmering geopolitical risks, a weaker U.S. dollar, and higher crude oil prices. Gold jumped to around 5,100 while silver climbed above 83, reflecting renewed investor interest despite recent volatility. U.S. Treasury Secretary Scott Bessent pointed to speculative activity by Chinese traders as a driver of extreme price swings, noting tightened margin requirements in China. At the same time, positioning data showed hedge funds and other money managers cutting bullish gold bets significantly after the metal suffered its steepest decline in more than a decade, suggesting the rally has been accompanied by heightened uncertainty and rapid shifts in sentiment.

Attention is now turning to a dense slate of U.S. economic data, including the January jobs report, consumer price index, retail sales, housing data, and agricultural supply figures, all of which could influence expectations for growth, inflation, and Federal Reserve policy. Payroll growth is expected to be modest, unemployment remains elevated relative to recent years, and core inflation is forecast to slow to its weakest pace since early 2021. Adding to market moves, Chinese regulators have advised banks to limit exposure to U.S. Treasuries to reduce concentration risk, a step framed as risk management rather than a loss of confidence, which weighed on the dollar and Treasury futures. Technically, gold and silver remain in bullish territory but face clear resistance and support levels that could define near-term direction. Source

Silver’s explosive surge above 120 per ounce was described as an unprecedented statistical anomaly, driven by a wave of short-term, crypto-style traders who approached the metal with extreme risk tolerance. According to RJO Futures senior broker Daniel Pavilonis, these participants treated silver like a momentum asset that could rise indefinitely, pouring money into deeply out-of-the-money call options that were extremely cheap when purchased. While experienced commodity traders also profited, they typically held smaller positions and managed risk by trimming exposure as prices rose, which limited their upside compared with newcomers who went all in on highly speculative bets.

As silver accelerated far beyond levels most professionals considered reasonable, seasoned traders reduced position sizes or exited futures altogether, effectively selling into demand from speculative buyers whose strategy was simply to stay long. This dynamic amplified the rally but also set the stage for the sharp reversal that followed, potentially worsened by large institutional short positions. After volatility peaked and prices collapsed, many YOLO traders gave back a significant portion of their gains, yet some still outperformed long-established professionals. The episode highlighted how disciplined risk management can lag during extreme market events, while aggressive speculation can deliver outsized rewards at the cost of equally outsized risk. Source

Image Source: Kitco News

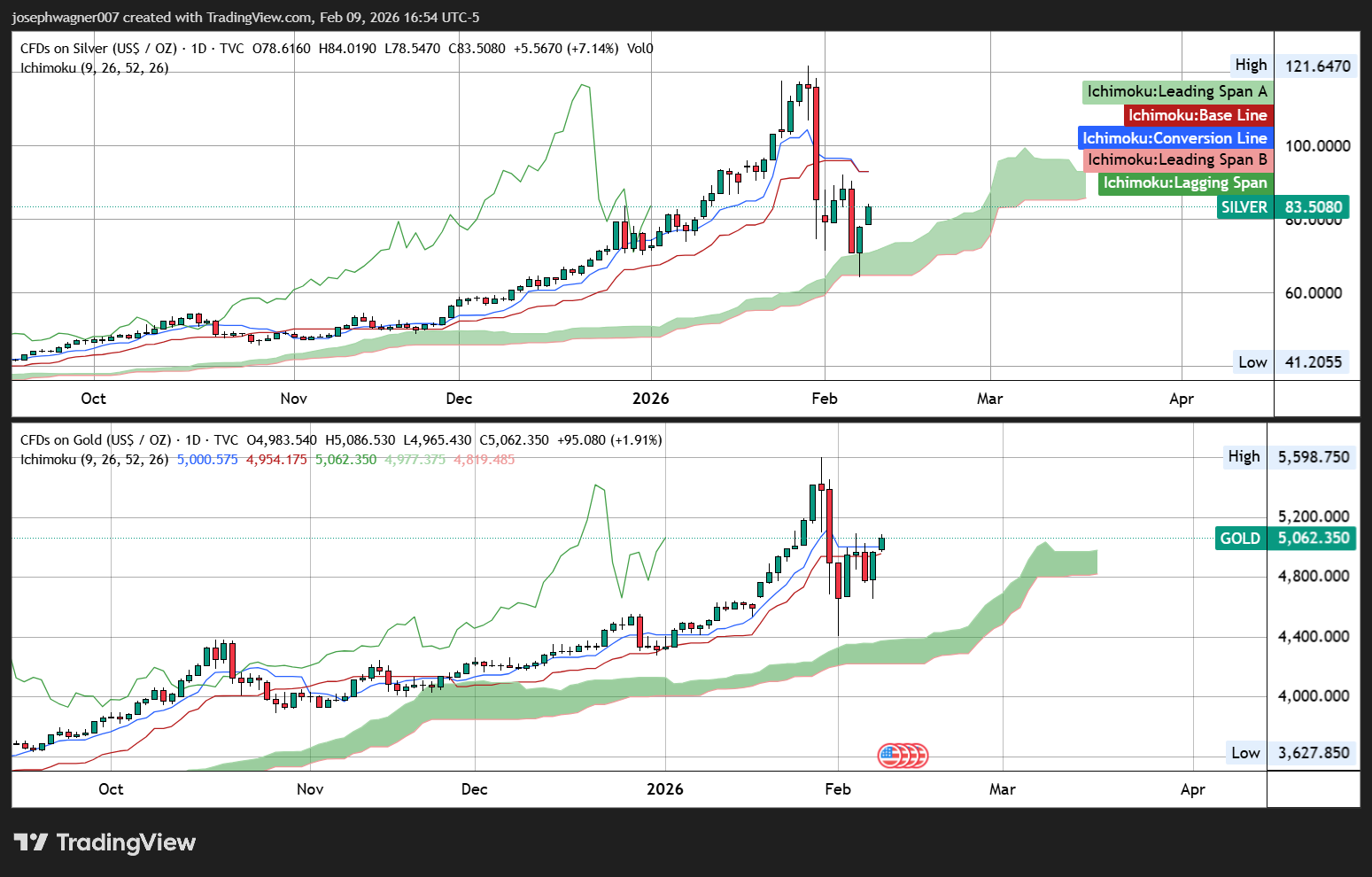

Gold and silver rebounded above critical technical levels, easing concerns that prices could become range-bound and suffer another pullback. Gold moved back above 5,000 after opening just below that mark, rising about 2% to around 5,063, while silver showed even stronger momentum by reclaiming 80 and climbing more than 7% to trade near 83.50. Silver’s sharper advance highlighted stronger bullish pressure compared with gold, as both metals invalidated near-term resistance levels that had been closely watched by traders.

The rally was supported by a notably weaker U.S. dollar, driven by growing expectations of soft economic data and increased scrutiny of upcoming releases including nonfarm payrolls, inflation, and jobless claims. Markets are already pricing in at least two interest rate cuts in 2026, adding further pressure to the dollar, which slid close to four-month lows. From a technical perspective, both metals remained above their Ichimoku cloud support on daily charts, signalling that their broader bullish structure remains intact. With key resistance levels now cleared and technical indicators still constructive, momentum points toward further upside in gold and silver through the remainder of the week. Source

Investment demand remains a key force in the gold market, with digital forms of exposure growing faster than traditional channels such as gold-backed ETFs. Analysts point to Tether and its gold-backed stablecoin, Tether Gold, as a major source of this shift, with the company estimated to hold between 125 and 150 tonnes of physical gold. This makes Tether the largest non-sovereign buyer of gold and places it among the top global holders, ahead of several national reserves. Gold also plays a broader role in Tether’s balance sheet, backing both its gold token and a portion of its U.S. dollar stablecoin reserves, with plans to increase that allocation further.

According to Société Générale, the scale and pace of flows into Tether Gold now rival those of the largest gold ETFs, even though it operates outside the traditional ETF structure. Its gold holdings would rank it as one of the largest ETF-like holders globally by tonnage, and recent inflows were among the strongest in the market, second only to the largest gold-backed ETF. These tokenized flows have increasingly influenced short-term price action, at times outweighing ETF demand and interacting with hedge fund positioning. During recent volatility, Tether added significant amounts of gold following a sharp selloff, reinforcing its role as an active and price-sensitive participant in the bullion market. Source

Gold and silver have shifted away from their traditional role as defensive assets and are now trading in a high-volatility, speculative environment, fundamentally altering the landscape for investors. Gold’s dramatic rise over the past decade, despite a largely unchanged dollar index, set the stage for sharp corrections as leveraged positions were unwound, stop losses were triggered, and margin requirements increased. Strong investment demand has been the dominant driver of prices, pushing total gold demand to a record 5,000 tonnes last year, even as jewellery and industrial demand weakened and central bank buying eased from record highs. This surge in speculative and investment-driven activity has left prices more vulnerable to rapid swings rather than steady, safe-haven behaviour.

Analysts expect heightened volatility to persist, noting that while gold has recovered a significant portion of its recent decline and moved back above 5,000, the earlier enthusiasm will likely take months to fully unwind, limiting the chance of new record highs in the near term. Silver has entered an even more volatile phase, with sharp rebounds and reversals driven by retail dip buying, large ETF inflows, and aggressive trading activity in China alongside rising margin requirements. Silver’s steeper declines have pushed the gold-to-silver ratio higher, underscoring its greater sensitivity on the downside, even as it follows gold higher in the latest rebound. Source

Gold staged a dramatic recovery after a violent early-week selloff, rebounding from lows near 4,450 and grinding higher to finish the week just below 5,000 per ounce. The week was marked by extreme volatility, with sharp overnight swings driven by alternating Asian and North American trading sessions, but prices ultimately stabilised as buyers defended key support zones around 4,600 to 4,800. By the end of the week, gold had shifted back into a more orderly bullish pattern rather than the parabolic behaviour seen previously, reinforcing the view that the selloff was a washout of leveraged positions rather than a fundamental trend reversal.

Sentiment surveys showed Wall Street analysts turning more optimistic after the rebound, while retail investors remained bullish but more cautious following recent losses. Most analysts expect continued choppy trading with an upward bias, as long-term drivers such as geopolitical risk, de-dollarization themes, and central bank demand remain intact, even as short-term risks persist around upcoming U.S. economic data including retail sales, nonfarm payrolls, jobless claims, and CPI. While some strategists warn that heavy selling could re-emerge near the 5,000 level, others see the recent pullback as a healthy reset within a longer-term bull market, with improved technical conditions, oversold signals, and negative retail sentiment pointing toward further recovery rather than a major top. Source

Gold outperformed other precious metals over the week, rebounding strongly from late-period weakness and demonstrating resilient investment demand despite higher futures margin requirements. Central bank buying remains a powerful structural support, with expectations for substantial purchases continuing into 2026 and renewed accumulation from countries such as Brazil and Poland. While silver lagged, analysts note that its long-term fundamentals are still underpinned by industrial demand, particularly from the solar sector, which is expected to absorb large volumes even as some jewelry manufacturers reduce silver usage in response to higher prices.

At the same time, heightened volatility has exposed vulnerabilities, especially in silver, where speculative demand has softened and the absence of central bank buying raises the risk of sharper pull-backs. Gold has already experienced a deeper correction than is typical during bull markets, leaving room for further downside if selling pressure intensifies, though longer-term confidence remains intact. Opportunities are emerging in the mining sector through acquisitions, expansion projects, and planned asset spin-offs, while threats include policy uncertainty around interest rates, liquidity-driven market swings, and shifting expectations about central bank independence, all of which could influence near-term price behaviour. Source

Sharp swings in gold and silver prices have unsettled investors, with daily moves reaching levels once associated only with crisis periods. Silver’s outsized fluctuations have intensified the sense of disorder, but the turbulence follows an exceptional rally in which gold set numerous record highs and silver became stretched. From this angle, the pullback looks like a natural correction rather than a breakdown, with gold now trading more comfortably within a broad range and still holding modest weekly gains despite the volatility.

Analysts argue the selloff reflects a release of speculative excess, not a change in gold’s long-term fundamentals. Prices have rebounded from recent lows, signalling resilient underlying demand driven largely by central bank buying and steady physical demand in major markets such as India and China. With institutional allocations still relatively low and macroeconomic risks unresolved, many bullish forecasts remain intact, supported by structural forces like rising debt, geopolitical tensions, and de-dollarization. Volatility is increasingly viewed as an adjustment phase that could set the stage for a more sustainable advance. Source

Gold and silver prices remain highly volatile after last week’s sharp selloff, with both metals struggling to regain stability below key resistance levels. Gold recorded one of the widest weekly trading ranges in its history, including an intraday plunge of more than 10% before rebounding, while silver experienced even more extreme moves, with daily swings far exceeding normal trading behaviour. Despite these sharp fluctuations, gold is modestly higher on the week and silver has seen intermittent buying interest, suggesting that while speculative excess is being unwound, prices are still finding support.

Analysts broadly agree that the turbulence reflects repositioning rather than a reversal of the long-term bullish trend. Structural drivers such as inflation concerns, shifting monetary policy expectations, geopolitical risks, and sovereign debt pressures remain intact, even as near-term downside risks persist. Many expect a period of consolidation or sideways trading to restore confidence after the recent frenzy, with forecasts still pointing to a potential return above 5,000 and even higher levels later in the year if supportive economic or geopolitical catalysts emerge. Volatility is expected to remain elevated as markets digest upcoming economic data and global political developments, reinforcing the view that this phase represents adjustment and caution rather than the end of the bull cycle. Source

Gold-backed exchange-traded products saw exceptionally strong investment demand at the start of 2026, even as prices suffered a sharp late-month selloff. Global gold ETFs recorded inflows of 120 tonnes worth nearly $19 billion in January, the strongest monthly inflow on record, lifting total holdings to a new all-time high of 4,145 tonnes. A sharp rise in gold prices earlier in the month also pushed the total value of ETF-held gold to a record $669 billion, with investors continuing to add exposure even during one of the steepest price declines in decades.

Asia led global inflows, accounting for more than half of total demand despite representing a much smaller share of global holdings, with China emerging as one of the largest sources of new investment. North American ETFs also posted strong gains, while European inflows were more modest but still positive amid economic and political uncertainty. The World Gold Council expects investment demand to remain a key pillar of the gold market in 2026, supported by low interest rates, persistent inflation, increased government spending, and ongoing geopolitical risks that continue to enhance gold’s appeal as a defensive asset relative to bonds. Source

Ted Oakley, founder of Oxbow Advisors, is warning that U.S. markets may face a significant correction of 10 to 15 percent as valuations clash with weakening economic fundamentals. Major technology stocks have surrendered nearly a trillion dollars in value, and jobless claims have risen to winter highs, signalling stalled corporate profit growth and rising layoffs. Oakley highlights the shift in tech companies’ business models from low-cost cash generators to capital-intensive investments, particularly in AI infrastructure, which has increased leverage and exposed investors to heightened risk. Meanwhile, consumers are financially stretched, with record credit card debt and rising delinquency rates limiting their ability to support economic growth.

Oakley advises investors to prepare for a volatile year, historically consistent with the second year of a presidential term, which often sees deeper intra-year drawdowns and muted returns. He recommends moving capital from high-flying tech stocks into defensive “stodgy” sectors such as pharmaceuticals and energy infrastructure while maintaining cash reserves to take advantage of market dips. Passive buy-and-hold strategies are unlikely to succeed in this environment, and he emphasises the need for selective, tactical investing, positioning for short-term volatility rather than relying on broad market momentum. Source

Video - "The Sobering Up Phase": Why Ted Oakley Says A 15% Sell-Off Is Possible

Federal Reserve Governor Stephen Miran argued that U.S. consumers are not the primary bearers of the Trump administration’s trade tariffs, asserting that foreign firms and their subsidiaries absorb most of the cost. Speaking at Boston University, Miran suggested that while initial fears predicted significant economic damage from the import taxes, the actual impact has been muted, and many economists have gradually aligned with his view. He noted that data can be misleading, as U.S. subsidiaries of foreign companies appear to show domestic burden, when in reality the costs are largely borne abroad.

Miran also highlighted that tariffs, combined with other government policies, are contributing to a more favourable long-term fiscal outlook by increasing revenue and helping reduce the primary deficit. While acknowledging that some research estimates Americans face higher costs—such as a Yale report placing the median household burden at around $1,400 annually—he maintained that the broader effect on U.S. inflation has been limited. The legality of the tariffs remains under Supreme Court review, with potential implications for their continuation and economic impact. Source

In this week’s Live from the Vault, Andrew Maguire reviews what he calls the largest derivative-driven intervention since 2008 before welcoming Craig Hemke, highlighting extreme margin hikes and record bid–offer spreads that hid severe shortages.

Despite the engineered sell-off, Shanghai premiums stayed high, speculative positions were cleared, and institutional buying continued, reinforcing Andrew’s view that gold and silver remain on track within a strong bull market amid currency debasement.

Disclaimer: These articles are provided for informational purposes only. They are not offered or intended to be used as legal, tax, investment, financial, or any other advice.

Featured Image - Source: Unsplash