x

Survey finds men more likely to consider life insurance because of the pandemic, as well as significant gaps in consumer knowledge on what life insurance does and how much is needed

May 26, 2020by Chris Moon

As the coronavirus pandemic continues to impact everything from the larger economy to daily life, it's exposed to many areas where we aren't nearly as prepared as we thought. For one, worries over personal safety have driven more interest in life insurance coverage. In a recent survey, ValuePenguin asked a nationwide sample of consumers about their thoughts on life insurance in the current situation.

When asked whether the coronavirus situation had influenced their likelihood of getting life insurance, 25% of consumers said it had made them more likely to do so. About 69% of those who responded positively were men, who also accounted for 38% of all men participating in the survey. In comparison, only 14% of all women said they were more likely to get coverage due to the pandemic.

These differences between men and women may be due to several factors. One possible reason is that while more and more women are assuming the role of the primary breadwinner, 59% of U.S. households still have a male family member earning at least half the household's income. Based on this, the higher interest in life insurance among men could be because men likely have a greater share of family income to protect.

Differences in opinion about coronavirus and life insurance also extended to current policyholders and those without coverage. People who already had life insurance policies were more likely to increase their insurance because of the pandemic(39%), compared to those with no coverage at the moment (20%).

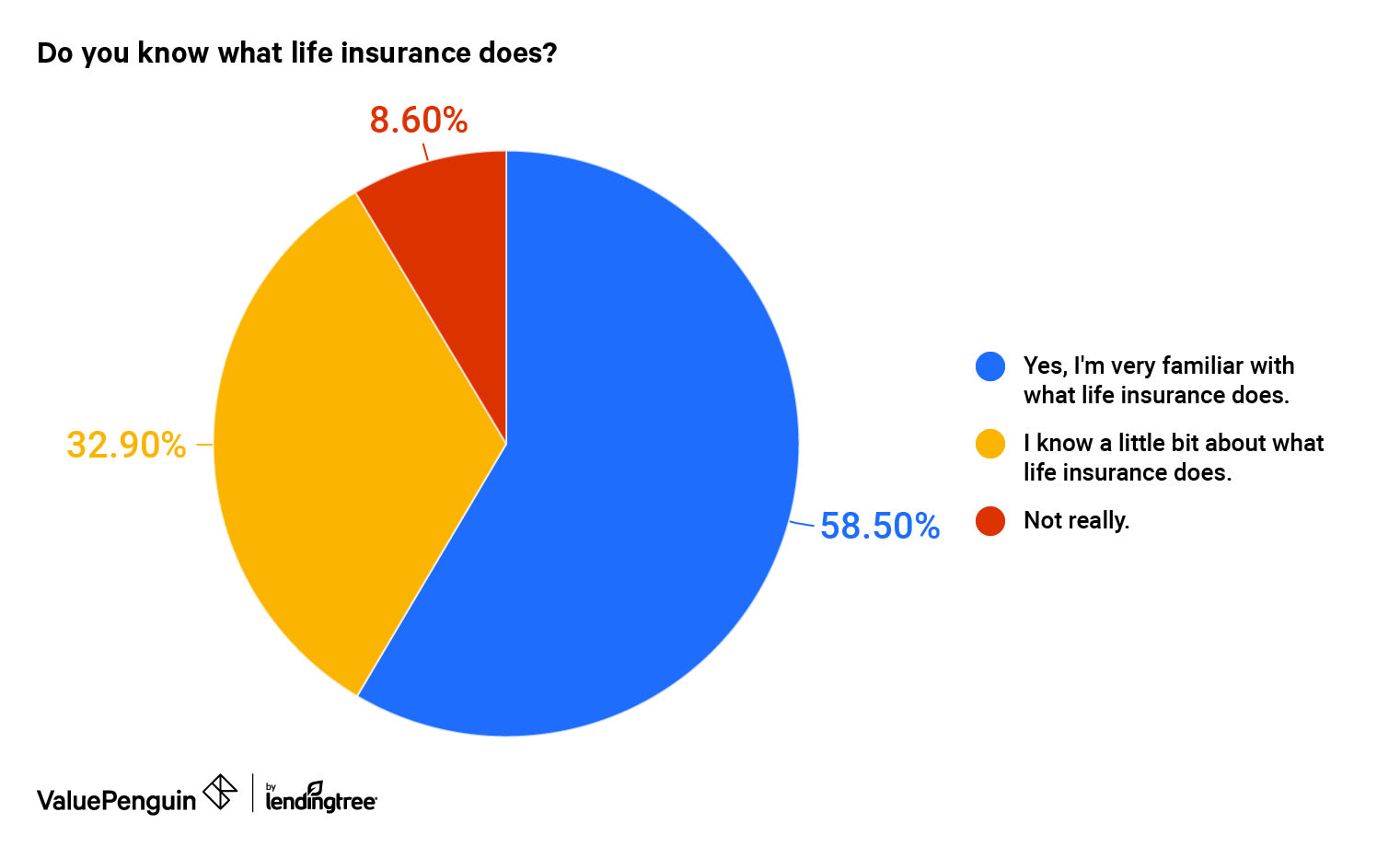

The survey results suggested more people want life insurance because of COVID-19, but they also revealed that a considerable number don't have much information about how life insurance policies work. While 65% of all respondents said they already had life insurance in place, only about 60% claimed they were "very familiar" with what life insurance does.

Meanwhile, 33% of people professed to "know a little bit" while 9% said they don't know what life insurance does. This relative lack of knowledge may be problematic, given the variety of policy types and benefits that make up the life insurance industry.

For example, the two most popular types of life insurance — term life and whole life insurance — differ widely in their pricing and benefits. Consumers must be informed about such differences in order to find the coverage that best fits their individual needs.

One of the most common questions regarding life insurance is how to calculate the proper amount of coverage. When asked how much life insurance is typically enough, 30% of consumers had no idea, while only 10% cited the common rule of thumb that coverage should be equal to 10 times your annual salary.

However, even that rule of thumb is often insufficient for an accurate estimate of a person's life insurance needs. Ultimately, the amount of coverage you have should be enough to meet all of your future financial obligations, minus the assets that would be liquidated on your passing.

Consider the example of a married homeowner with young children. In the event of an untimely death, the surviving spouse would be left to shoulder at least three ongoing financial obligations:

This list also excludes the one-time cost of a funeral, which typically costs around $10,000. While families are bound to cut back spending and adjust in such unfortunate cases, calculating your family's needs today and using that number to gauge your life insurance coverage can minimize the financial difficulty they would face without your support.

How much does life insurance cost?

The average cost of life insurance depends on your details, the type of policy, and how much coverage you're getting. As a baseline example, we've found that a $500,000 term life policy lasting 20 years would cost an average of $30 per month for a 35-year-old nonsmoker. Whole life insurance tends to be more expensive because it lasts your entire life and can also build cash value over time.

In most cases, we find that term life insurance is the most affordable and convenient way to obtain effective coverage. Unlike whole life policies and other types of permanent life insurance, a term life policy will not last forever. But it will last long enough to cover costs that eventually wind down, such as a mortgage or a child's college tuition. Check out our comparison of term and whole life insurance for more detail on which route may work best for you.

Calculating how much coverage you need leads to a unique result for every person. Some may want life insurance to cover the cost of supporting their children until adulthood, while others may also want to make sure their spouse receives support well into retirement.

At a minimum, you should start by adding up the lifetime cost of your current financial obligations, such as your mortgage and other payments on jointly held debt. Then add in the total cost of child care until your children reach adulthood, along with the amount you plan to contribute toward their college education.

Finally, you can subtract the value of your brokerage accounts, savings accounts, and any existing life insurance policies. Such assets can be liquidated to cover your family's needs on top of the payout from your new life insurance policy.

ValuePenguin commissioned Qualtrics to conduct an online survey of 1,136 Americans, with the sample base proportioned to represent the overall population. The survey was fielded between May 5 and May 8, 2020.

Chris is a Product Manager for ValuePenguin with years of experience in addressing critical questions about mortgages and homeowners' insurance. He spends his time evaluating insurance providers and policy features to understand where consumers might find the most cost-effective coverage. Chris has contributed insights to the New York Times and many other publications.