x

The Federal Reserve finds itself navigating an exceptionally perilous economic landscape. For months, market commentators have debated the timing and frequency of potential interest rate cuts. Yet, the narrative has shifted dramatically. A stubborn cocktail of sticky inflation, geopolitical instability, and surging energy prices has forced investors to confront a stark new reality: interest rate hikes are back on the table.

While this shift in expectations has created temporary headwinds for gold, the long-term structural case for the precious metal has rarely looked more compelling. According to Ryan McIntyre, President of Sprott Inc., the central bank is caught in a classic catch-22 situation, walking a tightrope with no easy exit strategy.

Ultimately, this monetary deadlock creates an environment where alternative safe-haven assets become essential.

The core dilemma facing policymakers is one of balance. To suppress inflation and keep it moving towards target levels, interest rates must remain elevated. However, keeping borrowing costs high for an extended period risks tipping the broader economy into a severe slowdown, destabilising equity markets, and crushing corporate valuations.

Conversely, cut rates too quickly to stimulate economic growth, and inflation risks reigniting, eroding purchasing power and undermining consumer confidence. This delicate balancing act has left markets incredibly volatile, with expectations swinging from multiple rate cuts to a virtual coin flip on whether rates will actually rise before the end of the year.

Yet, as pressing as the inflation-versus-growth debate is, a far more systemic danger is brewing beneath the surface.

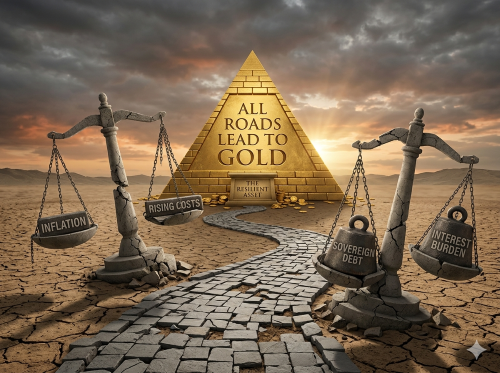

The most existential risk to the financial system isn't simply a temporary spike in consumer prices; it is the sustainability of sovereign debt. In major Western economies, and particularly in the United States, fiscal positions are deteriorating at an alarming pace. Government debt held by the public has climbed above 100% of Gross Domestic Product (GDP), reaching ratios not witnessed since the aftermath of the Second World War.

As national debt swells, the cost of servicing that debt rises alongside it. The financial system is fast approaching a critical tipping point where net interest expenses as a percentage of GDP will outpace nominal economic growth. When a nation's growth rate can no longer cover its interest obligations, policymakers lose almost all fiscal flexibility.

To attract investors to increasingly risky government bonds, the market will naturally demand higher real yields. However, the higher those bond yields climb, the greater the strain placed on the wider financial system. Richly valued equity markets, like the S&P 500, suffer immensely in high-yield environments, as future corporate cash flows are discounted at much harsher rates.

Bond markets are already beginning to signal discomfort with this trajectory. Investors are starting to demand a higher premium to compensate for the worsening fiscal outlook of Western governments.

This complex macroeconomic backdrop is precisely why gold remains an incredibly resilient asset class over the long term. In a scenario where confidence in sovereign debt erodes and central banks run out of credible policy options, physical assets with no counterparty risk become highly sought after.

If the Fed keeps rates high to combat inflation, it exacerbates the debt servicing crisis and punishes equities. If it lowers rates to ease the debt burden, inflation runs rampant. In both outcomes, traditional paper assets face significant structural risks. Gold, by contrast, thrives on the erosion of trust in fiat currencies and government bonds.

Furthermore, structural global shifts are creating a permanently more expensive operating environment for businesses. Deglobalisation, supply chain fragmentation, and the need for companies to build costlier operational redundancies mean that inflationary pressures could persist for years. This secular trend will likely eat into future corporate earnings, making equities less attractive on a risk-adjusted basis.

Intriguingly, despite gold trading near historic highs, broader investor participation remains surprisingly low. Global gold ETF holdings are well below their historical peaks, and institutional allocation to the precious metals sector is still remarkably muted. Wealth managers and large institutions have yet to fully rotate into the sector.

For forward-thinking investors, this lack of mainstream enthusiasm suggests that the market has not yet fully priced in the severity of the sovereign debt dilemma. Rather than viewing recent price consolidation or short-term volatility as a negative signal, many analysts view these periods as tactical opportunities to establish or build a core holding in precious metals.

As the policy options for central banks continue to narrow, the traditional pillars of a balanced portfolio are facing unprecedented challenges. When the choice comes down to inflating the debt away or risking a systemic financial slowdown, tangible, un-devaluable assets are poised to remind the market of their timeless utility.

For more detailed insights and the original discussion on this topic, visit the full report on Kitco News:

👉 Fed trapped between inflation and debt crisis, and gold wins either way - Sprott's McIntyre

Disclaimer: This article is provided for informational purposes only, mistakes may be made, and it's not offered or intended to be used as legal, tax, investment, financial, or any other advice.