x

Gold has struggled to break above $5,200 per ounce despite geopolitical tensions linked to the Iran conflict, reflecting a pattern seen in past wars where initial price spikes fade as investors prioritise liquidity and respond to interest rate changes. UBS analysts argue that gold’s muted reaction is typical, noting that its true strength lies not in immediate wartime demand but in hedging against broader economic consequences such as inflation, currency weakness and rising debt. Short-term pressures including a stronger US dollar, elevated energy prices and concerns over rate hikes have weighed on the metal, though UBS expects central banks to remain cautious rather than aggressively tightening policy.

Over the longer term, UBS maintains a bullish outlook, forecasting gold could reach as high as $6,200 per ounce by 2026, supported by strong structural demand and macroeconomic conditions. Continued central bank buying, resilient investment flows, and rising jewellery demand in Asia are expected to underpin consumption, while limited supply growth adds further support. The bank also highlights persistent geopolitical uncertainty, fiscal deficits and a likely easing cycle from the Federal Reserve as key drivers, reinforcing gold’s role as a portfolio diversifier and inflation hedge, with investors encouraged to maintain modest exposure within diversified portfolios. Source

Gold has struggled to gain traction despite heightened geopolitical tensions, with prices hovering near $5,000 as a liquidity-driven market environment limits its traditional safe-haven appeal. Christopher Vecchio of Tastylive explains that in the early stages of major crises, investors tend to prioritise cash, particularly the US dollar, over assets like gold. This pattern has been seen in past events such as the global financial crisis and COVID-19, where gold initially weakened before recovering strongly. While supply chain disruptions and rising energy-related risks are building in the background, they have yet to translate into sustained demand for the metal.

Vecchio remains positive on gold’s longer-term outlook but argues that traders should adapt their strategies to current conditions, favouring approaches that benefit from stability rather than immediate price surges. Instead of buying call options, which depend on strong upward momentum, he suggests selling put options to generate returns through time decay while maintaining bullish exposure. This strategy can perform even if gold trades sideways, though it carries greater risk if prices fall sharply. Once liquidity pressures ease and broader macroeconomic concerns take centre stage, gold is expected to regain stronger upward momentum. Source

Recent surges in oil prices have had little impact on longer-dated futures so far, but Sean Lusk of Walsh Trading warns that if the Iran conflict continues beyond mid-April, broader economic consequences could emerge across markets. He highlights a strong link between equities, metals and yields, noting that gold and silver have been moving in tandem with falling stock markets rather than acting as safe havens. Despite volatility, markets remain relatively stable for now, with no signs of panic selling in US assets, though sustained oil prices above $90 could begin to pressure economies and potentially force asset sales to cover rising energy costs.

Lusk explains that current pricing dynamics reflect logistical disruptions rather than true supply shortages, with much of the oil already sold and priced in, creating backwardation in the market. However, he cautions that conditions could shift quickly depending on how long the conflict lasts. In the near term, he expects further downside in precious metals as investors unwind positions built during years of equity-driven gains, suggesting gold could dip below $5,000 before recovering. He adds that a more attractive buying opportunity may emerge after markets fully adjust, at which point a stronger rally in metals could follow. Source

Gold has struggled to hold above $5,000 amid a stronger US dollar driven by geopolitical tensions and liquidity concerns, but Robert Minter of abrdn argues that investors are focusing on the wrong benchmark. He says the traditional relationship between gold, the dollar and interest rates has broken down since 2022, and that the metal should instead be assessed against the rapid expansion of global central bank balance sheets and the erosion of currency purchasing power. With balance sheets rising approximately tenfold since the late 1990s, gold’s long-term performance has mirrored this growth, reinforcing its role as a hedge against currency debasement and inflation.

Minter highlights persistent global debt and continued central bank buying as key drivers supporting gold’s long-term outlook, noting that meaningful declines in sovereign debt appear unlikely. Despite some moderation in physical purchases, higher prices have led central banks to allocate more capital to gold, underlining sustained demand. He maintains that the broader bull market remains intact, supported by geopolitical uncertainty and structural economic risks, and forecasts prices around $5,500 over the next year, with potential for further gains as hesitant investors re-enter the market. Source

Gold and silver prices declined around midday Monday, although they recovered slightly from earlier lows as improving risk appetite in wider markets reduced demand for safe-haven assets. A rebound in U.S. stock indices and a sharp drop in crude oil prices added pressure on metals, while concerns about inflation linked to the Middle East conflict also dampened buying interest. April gold fell by $56.30 to $5,005.30, while May silver dropped by $0.308 to $81.01. Sentiment shifted after comments from U.S. Treasury Secretary Bessent indicated oil tankers were moving through the Strait of Hormuz, easing supply concerns and prompting equities to rise and oil prices to fall.

Further influencing markets, the U.S. government initiated a large-scale release of crude oil from its Strategic Petroleum Reserve, with plans to distribute 86 million barrels as part of a broader 400 million-barrel international effort to lower energy costs. External market factors included a weaker U.S. dollar, crude oil trading near $95.50 per barrel, and a 10-year Treasury yield of 4.234 percent. Technically, gold and silver futures remain within defined ranges, with key resistance and support levels shaping short-term trading outlooks, while market ratings suggest moderately bullish conditions for gold and more neutral sentiment for silver. Source

Image Source: Kitco News

Gold has shown a misleadingly stable performance despite underlying weakness, as recent market movements reveal a divergence between safe-haven demand and price action. Following a coordinated U.S.-Israeli strike in the Middle East, both gold and the U.S. dollar initially surged, but gold reversed by the close while the dollar continued rising, signalling relative weakness. Crude oil displayed a similar pattern, with sharp early gains followed by intraday retracements, yet a consistent weekly rebound has emerged. Recent optimism over safe passage through the Strait of Hormuz has boosted sentiment, but Iran’s continued stance on controlling the waterway rather than fully reopening it highlights ongoing geopolitical risks that could sustain volatility in oil and related markets.

For gold, the apparent stability is partly an illusion created by a weaker U.S. dollar, which mechanically props up prices in nominal terms. When adjusting for currency effects, the metal’s performance is negative, suggesting the path of least resistance remains downward in the near term. Traders expecting a ceasefire-driven rebound may be misled, as a sustained rally in gold would require either a genuine de-escalation in the Strait of Hormuz or significant U.S. economic deterioration to revive rate-cut expectations, neither of which is currently apparent. The interplay between oil, the dollar, and geopolitical risk will continue to dictate gold’s trajectory over the coming week. Source

Historical analysis shows that wars causing oil price spikes tend to have limited direct impact on the direction of precious metals prices, with existing trends usually continuing. However, when such shocks lead to economic downturns, metals prices weaken significantly. Examples from the 1970s, the Gulf War, and more recent conflicts suggest that recessions, rather than geopolitical events themselves, are the main driver of declines. Current economic conditions appear fragile despite steady US growth, with weak jobs data and rising energy costs increasing pressure on businesses and consumers, raising the likelihood of a recession after an extended economic cycle.

A downturn would likely hit silver and platinum group metals harder than gold due to their heavier reliance on industrial demand, while expectations for US interest rate cuts have also been reduced בעקבות higher inflation linked to rising oil prices. Meanwhile, global developments such as India allowing greater investment in gold and silver could support demand, though silver investment trends remain mixed, with ETF holdings declining even as futures positions increase and coin sales show seasonal strength. Prices for both gold and silver continue to fluctuate around key levels, with silver facing downside risks if support zones fail. Source

Gold prices remained steady above the $5,000 level despite weaker-than-expected data from the New York Federal Reserve’s Empire State Manufacturing Survey, which slipped into contraction at -0.2 in March from 7.1 in February. The figure fell short of forecasts and highlighted ongoing struggles in the U.S. manufacturing sector, although the market reaction in gold was muted, with prices holding near $5,019 an ounce. While manufacturing activity showed signs of stabilising, issues such as longer delivery times and reduced supply availability persisted, even as overall business sentiment remained optimistic.

A closer look at the report revealed mixed underlying trends, with modest improvements in new orders and employment suggesting some resilience in the sector. However, shipments declined sharply, pointing to uneven demand conditions. At the same time, easing inflation pressures were evident as the prices paid index dropped significantly, reflecting a slowdown in cost increases. These mixed signals have kept gold trading in a neutral range, lacking strong upward momentum despite softer economic data. Source

Gold prices are facing short-term pressure after a recent rally, with the metal hovering near the $5,000 level as markets weigh slowing economic growth against persistent inflation. U.S. GDP growth has weakened significantly, while inflation remains elevated, reviving concerns about stagflation and complicating the outlook for investors. In the near term, the Federal Reserve’s reluctance to cut interest rates due to ongoing price pressures is supporting the U.S. dollar and bond yields, both of which tend to limit gold’s appeal and help explain its current consolidation.

Despite this near-term weakness, underlying conditions point to stronger long-term prospects for gold. Prolonged higher interest rates risk worsening an already fragile global economy, increasing pressure on government finances as debt levels rise and borrowing costs climb. At the same time, ongoing geopolitical tensions and structural risks in both equity and bond markets are reinforcing gold’s role as a diversification asset for institutional investors. The current dip in prices is therefore seen as a temporary phase, with broader economic and market forces continuing to support gold’s longer-term trajectory. Source

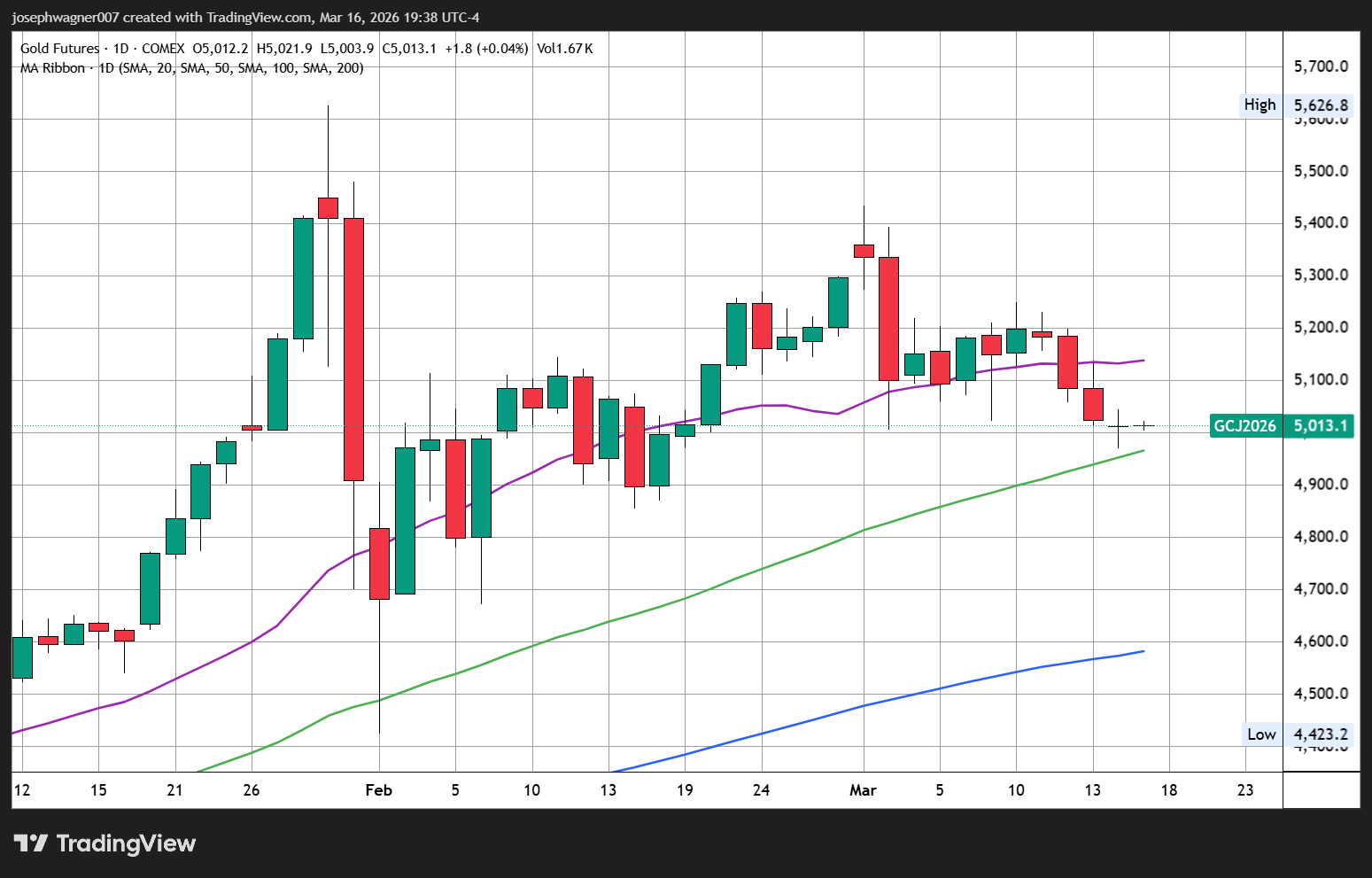

Gold traded within a wide but defined range between $5,000 and $5,240 over the week, initially rising before falling back as concerns grew about a prolonged Middle East conflict and its impact on global markets. Despite several attempts to break higher, prices repeatedly met resistance above $5,200 and drifted lower towards key support near $5,000. Analysts remain divided on the short-term outlook, with Wall Street showing an even split between bullish and bearish expectations, while retail investors maintain a modestly positive bias. Market sentiment is being shaped by uncertainty around the Federal Reserve’s upcoming decision, geopolitical developments, and the interaction between equities, bond yields and energy prices.

Many analysts highlighted that gold is currently moving in tandem with equities and reacting to shifts in yields and oil prices, rather than behaving as a traditional safe haven. Rising yields and a stronger dollar are putting pressure on prices, while ongoing geopolitical tensions and potential changes in oil flows continue to add volatility. Some expect further downside in the near term, particularly if interest rates remain elevated or equity markets weaken, although others see support holding firm around $5,000 as a sign of underlying strength. Overall, markets are in a holding pattern, waiting for clearer signals from central banks and developments in the Iran conflict before determining gold’s next direction. Source

Gold is experiencing short-term pressure as the dollar strengthens ahead of the Federal Reserve’s upcoming monetary policy meeting, with spot prices testing support above $5,000 an ounce. Silver is showing similar weakness, trading around $81 an ounce. Analysts attribute the selloff not to a lack of safe-haven demand, but to a liquidity-driven environment where investors are prioritising U.S. dollars amid the U.S.-Israel conflict with Iran and broader market uncertainty. Rising Treasury yields and elevated oil prices are also contributing to pressure on precious metals, keeping near-term risks skewed to the downside.

Despite the immediate weakness, many experts remain cautiously optimistic about gold’s longer-term outlook. Geopolitical tensions, persistent inflation, and growing sovereign debt levels are expected to continue underpinning demand, while potential future Fed rate cuts could provide further support once the liquidity crunch eases. Markets are focused not only on the U.S. central bank but also on upcoming decisions from major global central banks, alongside key economic indicators such as manufacturing surveys, housing data, and producer inflation. Analysts suggest that while gold may test lower levels near $5,000 or $4,900 in the short term, the metal’s long-term fundamentals remain robust. Source

The current rally in gold has largely bypassed equities so far, creating a significant opportunity for investors in gold mining stocks. The surge in gold prices was initially driven by central banks accumulating physical gold rather than by equity investors, leaving mining shares historically undervalued relative to the metal and broader markets. Geopolitical tensions, economic uncertainty, and trade disputes have recently shifted attention back to gold, positioning mining equities as a potentially high-upside segment of the market. The sector’s small size means even modest portfolio allocations could significantly influence stock prices, while large-cap producers are attracting initial investment before capital moves to smaller developers and explorers.

Ninepoint Partners is structuring its portfolio to capture this potential, balancing investments between established producers and junior mining companies that could benefit from future growth. Producers offer strong cash flows and shareholder returns but face limited organic growth, which could drive acquisitions and support juniors. Even if gold prices remain stable, Wachowiak expects mining equities could double due to robust margins and increasing investor interest. Longer-term structural factors, including geopolitics, technological advances, and the global energy transition, are also expected to sustain demand for metals, making the current phase of the gold mining cycle an opportunity that could unfold over the next decade. Source

In this week’s Live from the Vault, Andrew Maguire reveals how war headlines and a dollar spike are masking deeper drivers for precious metals: private credit stress, mounting stagflation, and accelerating sovereign accumulation of physical gold.

With Asian markets absorbing Western supply and silver inventories reaching historically low levels, Andrew outlines how global wealth rotation into physical gold and silver could trigger a dramatic repricing across the precious metals market.

In this episode of Live from the Vault, Andrew Maguire discusses the growing dislocation between paper-based western markets and the physical precious metals exchanges in the East, particularly the Shanghai Gold Exchange. He argues that while mainstream media focusses on war-related volatility and the strength of the dollar, the underlying drivers for gold and silver are actually found in private credit instability and a global shift towards de-dollarisation. Maguire explains that major bullion banks are beginning to align with Eastern hubs like Singapore and Shanghai to access physical supply, suggesting that the legacy price-setting mechanisms in London and New York are losing their influence. He concludes that as central banks and institutional investors move from minimal to significant allocations in physical metals, current prices represent a closing window of opportunity for investors to protect their wealth against currency debasement and systemic financial risks.

Disclaimer: These articles are provided for informational purposes only. They are not offered or intended to be used as legal, tax, investment, financial, or any other advice.