x

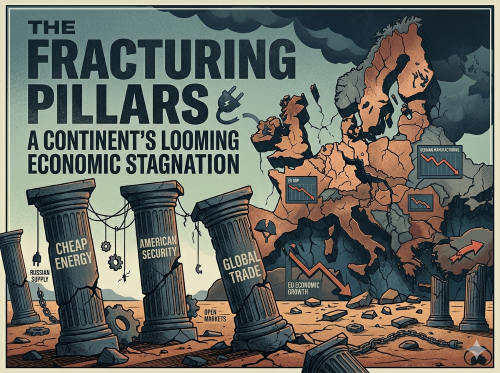

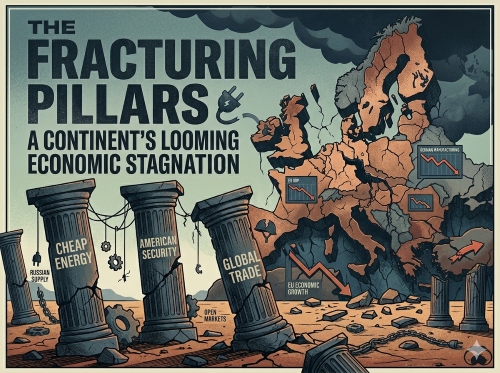

For nearly forty years, the European economic architecture functioned smoothly on three unwritten rules: access to affordable Russian energy to power major manufacturing hubs, protection under the American security umbrella to offset domestic defence spending, and open global trade markets to consume high-value exports. However, recent geopolitical and macroeconomic developments indicate that these foundational pillars are rapidly fracturing, leaving the European Union to confront a highly complex economic reality.

Recent economic projections point to a sharp deceleration in growth across the bloc. According to the European Commission's spring 2026 forecast, the overall gross domestic product growth projection for the EU has been lowered to 1.1 per cent, down from 1.5 per cent in the previous year. The outlook within the Eurozone is even more subdued, with growth adjusted downward to 0.9 per cent. This slowdown is actively occurring at a time when traditional growth engines are experiencing severe structural challenges rather than temporary cyclical downturns.

Germany, long considered the industrial powerhouse of Europe, is experiencing a profound structural shift. The German Council of Economic Advisers and the Ifo Institute have noted that declining industrial competitiveness and an ageing workforce are fundamentally reshaping the nation's economic landscape. In April 2026, German unemployment crossed above three million for the first time in fifteen years, pushing the seasonally adjusted unemployment rate to 6.4 per cent.

This shift is highly evident in the manufacturing and automotive sectors. Since 2019, German industry has shed over 340,000 jobs, representing roughly six per cent of its entire industrial workforce. Major corporate restructuring efforts are underway across the country, with heavy industrial and automotive champions reporting steep declines in quarterly net profits. As domestic production becomes less competitive, foreign direct investment has followed a downward trajectory, declining for eight consecutive years to reach a seventeen-year low.

The economic cooling is not confined to Germany. France recently recorded flat business activity, with indicators hitting multi-year lows. Meanwhile, Ireland, which previously led the bloc in rapid economic expansion, has experienced a sharp correction, moving from double-digit growth to a projected contraction. The European Commission has described the current macroeconomic environment as a stagflationary shock, indicating a difficult combination of slow growth and persistent underlying cost pressures.

The loss of low-cost energy inputs remains a primary driver of Europe's industrial challenges. Industrial electricity prices within the European Union are currently more than double those found in the United States and approximately 50 per cent higher than in China. Ongoing international conflicts continue to introduce volatility into commodity markets, further widening the continent's energy deficit.

The real-world consequences of these sustained energy price discrepancies are visible in the widespread idling of industrial capacity. Between early 2024 and early 2026, over one hundred chemical facilities shut down operations across Europe, resulting in the loss of tens of thousands of manufacturing jobs and millions of tonnes of production capacity. Rather than reinvesting domestically, prominent European chemical and industrial conglomerates are shifting their capital focus abroad, opening multi-billion-pound mega-complexes in markets like China and North America where operational costs are significantly more predictable.

Beyond traditional manufacturing, Europe faces a growing productivity deficit driven by a widening technology gap. The vast majority of the world's leading technology firms are based outside of Europe, with the United States producing a significantly higher volume of new tech companies valued over one billion dollars.

A substantial portion of the per capita gross domestic product gap between the EU and the US is attributable to this lag in technological productivity. While regional scale-up funds exist, their total capitalisation remains small compared to the vast pools of venture capital available in North America. Consequently, many promising European startups routinely choose to incorporate abroad or sell to foreign buyers before achieving significant scale.

Furthermore, administrative and regulatory friction continues to slow down local implementation of major initiatives. For instance, the enforcement of flagship tech regulations, such as the AI Act's high-risk provisions, has faced multi-year delays. This is largely because a majority of member states missed deadlines to establish national contact points or issue necessary technical guidance, demonstrating the administrative challenges of coordinating complex policies across a fragmented twenty-seven-nation bloc.

Defence spending is one area where European nations have significantly increased their fiscal commitments. Total European military spending has risen sharply, marked by major multi-billion-pound regional readiness initiatives. However, this sudden influx of capital has encountered immediate supply chain bottlenecks and strategic misalignment.

A substantial percentage of European military equipment procurement still flows directly to external suppliers, primarily in the United States. Joint regional projects, such as next-generation fighter aircraft programmes, are showing signs of political and corporate splintering as individual nations explore independent procurement routes or alternative partnerships.

Simultaneously, domestic capital within Europe remains highly underutilised. Approximately eleven trillion euros currently sits dormant in European household savings accounts, earning minimal returns. This immense pool of wealth, which exceeds the combined annual GDP of Germany and France, remains frozen in cash due to the lack of a unified financial architecture. Cross-border investment within the bloc remains incredibly complex because savers must navigate twenty-seven distinct national insolvency regimes, tax frameworks, and pension systems.

Efforts to establish a unified Savings and Investments Union remain slow due to resistance from smaller member states, who express concern over policy changes driven predominantly by the bloc's largest economies. As regional public deficits rise and average debt-to-GDP ratios head upward, the window for implementing deep structural reforms continues to narrow, leaving the average citizen to navigate a landscape of higher taxes, elevated energy bills, and stagnant real wage growth.

Coin Bureau - Europe is Collapsing

"Europe’s economy is unraveling. Growth forecasts are sinking, industrial jobs are being slashed, and energy costs keep climbing. The European Commission’s Spring 2026 Forecast paints a bleak picture, with political disputes and red tape making real fixes almost impossible.

Trillions in savings sit idle while the gap with the US and China widens. Ordinary investors and workers now face falling markets, unpredictable taxes, and a weaker currency. Find out what’s really at stake for your money and future."

~ TIMESTAMPS ~

0:00 - The Collapse of Europe: 2026 Economic Warning

3:01 - Germany's Crisis: Engine of Europe Stalls

6:05 - Energy Shock: Why European Industry is Fleeing to China

9:08 - The Innovation Gap: Why Europe is Losing the Tech War

12:12 - Military Fractures: The Splintering of European Defense

15:16 - Saving Your Wealth: The High Cost of Fiscal Decline

17:45 - Europe's Final Verdict: Can the Decline Be Reversed?

Source 👉 https://www.youtube.com/watch?v=3jMCbEo4EbU

Disclaimer: This article is provided for informational purposes only, mistakes may be made, and it's not offered or intended to be used as legal, tax, investment, financial, or any other advice.