x

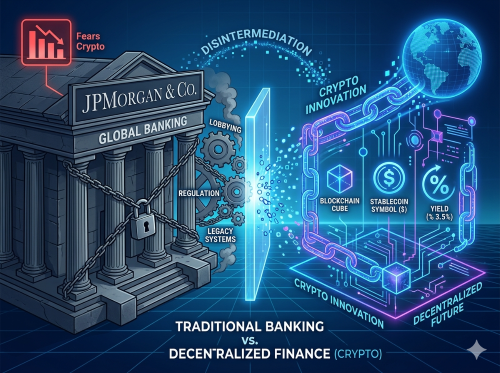

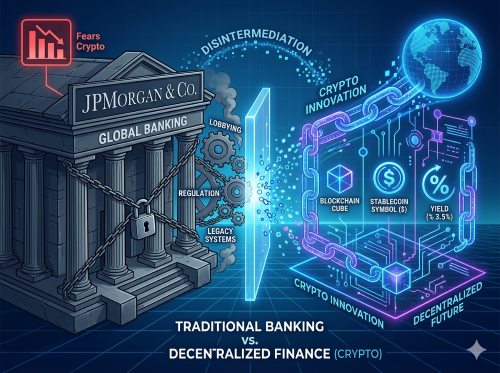

The traditional financial landscape is experiencing a profound undercurrent of friction. Publicly, the leaders of traditional banking present a united front of skepticism towards cryptocurrency, framing digital assets as unstable, risky, and inherently dangerous to the average consumer. However, a deeper look behind the scenes reveals a fascinating contradiction. While major financial institutions lobby aggressively to restrict cryptonative products, they are simultaneously racing to build and deploy the exact same technology within their own walls.

This tension recently escalated into open conflict. Prominent banking executives have stepped directly into the media spotlight to declare a regulatory war against digital assets, specifically targeting the legislative progress of stablecoin frameworks like the Clarity Act. The public argument is simple: yield-bearing stablecoins threaten financial stability and consumer safety. Yet, the internal actions of these very same banks tell a completely different story—one driven by the fear of losing control over the world's financial rails.

The public opposition from traditional banking circles is focused heavily on the concept of yield-bearing stablecoins—digital assets pegged to the US dollar that pass treasury yields directly back to the holder. In high-profile media appearances, banking leaders have argued that if crypto firms can offer interest-like returns on digital dollars without facing traditional banking regulations, it could trigger a massive exodus of deposits from commercial banks.

This argument has been amplified by powerful lobbying groups, including the American Bankers Association. These organizations have launched extensive campaigns, flooding lawmakers with letters warning that a mass migration of deposits into payment stablecoins would drain liquidity from local institutions. The narrative warns that such a shift could severely restrict the ability of community banks to fund local business loans and mortgages, ultimately hindering macroeconomic growth. On paper, it is framed as a crusade for economic stability and consumer protection.

Despite the dire public warnings about the dangers of decentralized finance, the internal strategies of these banking giants paint a starkly different picture. The very institutions leading the charge against crypto are quietly investing billions of dollars to establish their own presence on public blockchains.

A prime example is the emergence of institutional deposit tokens. In a move that surprised many industry observers, major banks have launched their own digital tokens on public Ethereum layer-2 networks—the exact same infrastructure developed by the cryptonative companies they publicly critique. Furthermore, these institutions are actively filing paperwork to launch tokenized money market funds and blockchain-native treasury products designed to pass yields directly to qualified institutional investors.

The data highlights the scale of this commitment. Institutional blockchain platforms are already processing billions of dollars in transaction volume every single day. With technology budgets for major banks rising steadily, a significant portion of capital is being directed toward building out proprietary blockchain infrastructure. The contradiction is clear: the technology deemed too dangerous for the public is being actively embraced as the future of institutional finance.

If the technology is inherently sound enough for multi-billion-dollar bank settlements, the public panic cannot truly be about safety or financial instability. Instead, the real threat is disintermediation—the removal of the traditional middleman.

Commercial banks rely heavily on a base of cheap deposits, often paying everyday customers mere fractions of a percent on standard checking accounts. This low-cost capital is the raw material that funds profitable lending operations. Cryptonative alternatives disrupt this model entirely. When digital asset platforms allow users to earn competitive market yields on digital dollars, the traditional banking proposition loses its appeal.

The fear keeping banking executives awake at night is not that the financial system will collapse, but that consumers will realise they can bypass traditional commercial banks entirely to achieve better returns. The strategy, therefore, is not to eliminate digital dollars, but to control them. By using regulatory influence to create high barriers to entry, traditional finance aims to lock out cryptonative competitors. This allows banks to buy the time necessary to replace decentralized alternatives with their own centralized, proprietary versions.

This behind-the-scenes tug-of-war has had a direct impact on the speed of regulatory clarity. Bipartisan stablecoin legislation, which initially enjoyed strong momentum and passed through key committees, has faced significant delays. This slowdown is a direct result of intense lobbying from the traditional banking sector, which seeks to remove or alter provisions allowing non-bank stablecoin issuers to offer yield.

The constant friction has caused confidence in near-term legislative success to waiver. Industry insiders warn that if comprehensive frameworks fail to pass in the current legislative session, the window for clear rules could be pushed back by several years. This would leave a multi-billion-dollar digital asset market stranded in an environment of regulation by enforcement, creating prolonged uncertainty.

Ultimately, the aggressive pushback from traditional finance is not a demonstration of strength, but a revelation of vulnerability. Financial institutions do not deploy massive lobbying infrastructure to fight something irrelevant. They do so when they recognize a genuinely transformative technology that threatens their market dominance—and when they intend to own the infrastructure that replaces it.

Coin Bureau - Why JPMorgan Fears Crypto More Than Ever

"Jamie Dimon says yield-bearing stablecoins threaten financial stability and could ""blow up."" But while banks blast crypto in public, JPMorgan is quietly tokenizing yields on blockchain for its own clients using Coinbase’s network.

This video uncovers why JPMorgan is racing to dominate the very thing it claims is a risk, how the banking lobby is trying to freeze out crypto-native competitors, and what this all means for US law and the control of digital dollars. Watch before the next round of regulation lands."

~ TIMESTAMPS ~

0:00 - Jamie Dimon's War on Crypto & the Clarity Act

2:02 - Why Banks Fear Yield-Bearing Stablecoins

4:04 - JP Morgan’s Secret Crypto Project Exposed

6:07 - The Trillion-Dollar Tech Behind JPM’s Blockchain

8:10 - The Truth About Stablecoin Yields & Bank Lending

10:13 - Is the Clarity Act Stalled? The Future of Crypto Regulation

Source 👉 https://www.youtube.com/watch?v=xQLwEusHCmc

Disclaimer: This article is provided for informational purposes only, mistakes may be made, and it's not offered or intended to be used as legal, tax, investment, financial, or any other advice.