x

The gold market maintains its strong position above $3,800 an ounce, despite the latest U.S. labor market data indicating stabilization rather than significant weakening. The Labor Department's JOLTS report showed that job openings in August slightly increased to $7.23 million, which was generally in line with expectations and did not provoke a strong reaction in gold prices; instead, some volatility emerged as investors engaged in profit-taking after the price hit $3,870 overnight. Some analysts suggest that to push gold toward the $4,000 mark, the market may need to see more substantial signs of weakness in the labor sector.

While the number of job openings remains low, the relative stability—with hires and separations, including quits and layoffs, largely unchanged—may influence the Federal Reserve’s future actions. Analysts note that continued stabilization could make the Fed less inclined to aggressively cut interest rates, even after restarting its easing cycle. This employment report is also potentially the last one investors may see for a period due to Congress's failure to pass funding legislation to keep the government operational. Source

Market strategist Robert Gottlieb believes gold's recent rally to over $3,800 an ounce is unparalleled and suggests the precious metal has become a "force of nature" due to unprecedented geopolitical and economic uncertainty. He does not offer a specific price target but expects the bull run to last at least three more years, attributing its strength partly to global reactions to rising volatility stemming from deglobalization, trade wars, and political pressure on the US Federal Reserve. Gottlieb argues that the U.S. government's "weaponization" of the dollar against Russia in 2022 began a trend of nations diversifying away from the dollar, a move that intensified under current trade policies. This has structurally changed gold's status from a safe-haven asset to the "ultimate safe-haven asset" because it is not a fiat currency or dependent on the credit of any specific country.

The growing lack of faith in the U.S. dollar and Treasuries means central banks will continue to buy gold, even at record-high prices, according to Gottlieb. He notes that gold has already surpassed the euro as the second-largest asset held by central banks. While emerging market central banks have been the most active in acquiring gold, he believes it is only a matter of time before developed economy central banks follow suit, as central banks typically have deep pockets and price is not a primary concern when meeting long-term targets. China is highlighted as a significant factor, not only as the biggest source of demand and supply, but also as it seeks to become a global gold hub to rival London and New York. This strong, long-term central bank demand provides security for retail investors, whose participation in the rally is just beginning as they seek gold's insurance-policy value amid global uncertainty. Source

India's gold and silver imports nearly doubled from August to September, despite record-high prices for both metals. This surge was driven by banks and jewelers rushing to build up inventories ahead of the upcoming festival season, particularly Diwali in October, and in anticipation of a likely increase in the base import fees at the end of the month. The Indian government revises this base import price, which is used to calculate import duty, every 15 days, prompting a last-minute scramble to clear large amounts of gold and silver from customs before the expected tax hike. One government official noted that the rush hasn't been seen in years. In August, India spent $5.4 billion to import 64.17 tons of gold and $451.6 million on 410.8 tons of silver, and preliminary data suggests September figures will be substantially higher.

Jewelers who had previously held off on buying, hoping for a price correction, were forced to pay a premium to stock up, with domestic dealers charging up to $8 per ounce over official prices. This strong demand from India is surprising the international market, especially given that China, another major consumer, is remaining inactive at these price levels and has even seen dealers offering steep discounts. While spot gold and silver prices have shown volatility, reaching highs of $3,871.89 and $47.174 per ounce respectively before pulling back, the sustained import volume could negatively impact India's currency and widen the country’s trade deficit. Source

BMO Capital Markets has significantly upgraded its price forecasts for gold and silver, driven primarily by mounting concerns over rising Western sovereign debt, particularly in the U.S. The bank projects that gold will average $3,900 an ounce in the fourth quarter of 2025, and believes the rally will push prices above $4,000 next year. This long-term bullish outlook sees gold averaging $4,400 an ounce in 2026 and settling at a new long-term average of $3,000 an ounce, up sharply from previous estimates. BMO argues that while geopolitical turmoil, sticky inflation, and de-dollarization have all contributed to gold’s rally, the core driver is the unsustainable growth in government debt, leading investors to seek gold as a hedge against the long-term devaluation of fiat currency. This has moved gold investment into the mainstream for a broader set of risk-tolerant investors.

While remaining extremely bullish on gold, BMO expects silver to outperform through the end of the year, forecasting prices to average around $45 an ounce in the fourth quarter of 2025, a 41% increase from its prior estimate. The bank anticipates the silver rally to continue, with prices hitting $50 an ounce in the second quarter of 2026 and averaging $49.50 for the full year. This strong outlook is supported by silver's typical linkage to gold's fortunes, but also by robust industrial demand, specifically its crucial role in photovoltaics and power grids as part of the energy transition. BMO expects a persistent supply deficit for silver, which will require prices to remain elevated to draw material from existing investment stockpiles into industrial inventories. Source

Gold prices are seeing continued upward momentum, currently trading at $3,889.46 per ounce, driven by a convergence of market uncertainty, rising geopolitical tensions, and recent U.S. economic data that is boosting demand for the safe-haven asset. Significant factors contributing to this trend include aggressive political rhetoric and rising fears of a potential U.S. government shutdown, which together are injecting a considerable risk premium into the market. The latest U.S. ADP Non-Farm Employment Change for September was significantly lower than expected, pointing to weakness in the labor market and a slowing economy. This data increases the likelihood that the Federal Reserve may adopt a more cautious or dovish stance, pausing or easing its tightening cycle, which would make gold more attractive as real bond yields could remain low.

The weak employment data, combined with mixed signals from the ISM Manufacturing PMI—which showed the sector remains in contraction but with persistent inflationary pressures in the industrial sector—creates a complex picture for the Fed's next steps. While inflation remains a concern in some areas, the overall slowdown in jobs and manufacturing output is intensifying market expectations for rate cuts, further strengthening gold’s appeal as both an inflation hedge and a safe-haven asset. Additionally, the increasing threat of a U.S. government shutdown, which would introduce significant market uncertainty and economic disruption, is another critical factor pushing capital inflows into gold, as investors seek protection from potential policy paralysis and delays in essential economic reporting. Source

The gold market experienced a dip after private sector payrolls processor ADP released its latest employment data, revealing a surprisingly weak U.S. labor market. The report indicated that 32,000 jobs were lost in September, significantly missing the consensus forecast which had expected a gain of 50,000 jobs. This job loss validates concerns that U.S. employers are cautious about hiring, despite strong economic growth earlier in the year. The losses were concentrated mostly in the service-providing sector, which shed 28,000 jobs, with the goods-producing sector losing a further 3,000. Annual wage gains for those who stayed in their jobs were little changed at 4.5%, but pay increases for job-changers slowed down.

Given that a potential government shutdown could delay the release of the official government jobs report, financial markets are paying more attention to this ADP data than usual. This weaker-than-expected jobs report is seen as increasing the likelihood of the Federal Reserve adopting a more accommodative monetary policy, specifically making it more probable that the Fed will cut the federal funds target rate by another quarter percent at its upcoming October meeting. This expected policy move is intended to help stimulate the economy and consumption, particularly benefiting workers in the lower half of the income distribution as the labor market tightens. Source

The gold market is maintaining strong gains near record levels despite a lack of significant reaction to recent weak economic data concerning the US manufacturing sector. The Institute for Supply Management's Manufacturing Purchasing Managers Index (PMI) for September showed a slight increase to 49.1, up from 48.7 in August. While this modest improvement was in line with expectations, the reading remains below the critical 50-point threshold, marking the seventh consecutive month of contraction in the manufacturing sector. A large percentage of the sector's gross domestic product continued to contract, with a notable increase in the portion that is strongly contracting, indicating persistent weakness. Despite this economic backdrop, spot gold last traded around $3,870.20 an ounce, showing a modest daily gain of 0.32%.

Examining the components of the ISM report reveals mixed signals within the manufacturing economy. The New Orders index fell to 48.9, a drop from the previous month, suggesting softening demand, while the Production Index rose to 51, signaling an uptick in output. Furthermore, the report pointed to a modest positive trend in the labor market, with the Employment Index increasing to 45.3. A key takeaway is the easing of inflationary pressures, as the Price Index dropped to 61.9 from 63.7 in August, suggesting that contracting activity is leading to lower prices for manufactured goods. Source

StoneX's Head of Market Analysis, Rhona O’Connell, analyzed the potential effects of the fifth US Federal government shutdown in 30 years by reviewing the causes and market impacts of the previous four. Unlike a debt ceiling issue, this shutdown is due to a political impasse over passing Appropriations Bills, specifically related to funding for Health & Human Services, though it affects up to twelve government agencies. The current political debate includes the possibility of permanent lay-offs for federal employees instead of temporary suspensions, a follow-through on the desire to reduce government payroll levels. Historically, a shutdown can also impact economic data releases, such as delaying the Non-Farm numbers if the Bureau of Labor Statistics is affected. O’Connell’s analysis looked at market performance during shutdowns under Presidents Clinton (two), Obama, and Trump, focusing on gold, 2-year Treasury yields, the S&P 500, and the US dollar index.

Reviewing the previous four shutdowns, the market impacts varied, though a common thread was political wrangling over spending or policy issues like Medicare, the Affordable Care Act, or border wall funding. During the two Clinton-era shutdowns, gold underperformed stocks in the five-day event, but overall market reaction was mixed. The 16-day Obama-era shutdown saw a relatively muted market reaction, with gold, the dollar, and the S&P holding steady, while 2-year Treasury yields spiked early before falling. The longest shutdown under President Trump (35 days) saw 2-year Treasury yields and the dollar weaken, while gold and the S&P 500 rose, with stocks significantly outperforming gold. The initial market reaction to the latest shutdown has seen the US 2-year yield fall the most, with the dollar weakening slightly, and gold and the S&P 500 showing modest gains. Source

Gold and silver prices surged in midday US trading on Wednesday, driven by safe-haven demand following the US government shutdown and a weak monthly US ADP jobs report, which fueled speculation for lower interest rates sooner. Gold reached a record high of $3,894.40 per ounce for the December futures contract and is now approaching the $4,000 mark. The metal has soared over 48% this year, putting it on track for its best annual performance since 1979. The government shutdown, triggered by a stalemate over health care subsidies, is the first in nearly seven years and could be prolonged, potentially disrupting public services, delaying key economic data like the upcoming Labor Department employment report, and impacting hundreds of thousands of Americans' jobs.

Silver prices also posted sharp gains, with December futures hitting a 14-year peak at $47.585 an ounce and closing in on its all-time high of just over $50.00 from 1980. Technically, both gold and silver futures contracts currently show a strong overall near-term technical advantage for the bulls, with both markets receiving a high Wyckoff's Market Rating of 9.0. Outside markets saw the US dollar index nearly steady, crude oil prices weaker around $62.00 a barrel, and the 10-year US Treasury note yield around 4.15%. Bulls' next major upside objective for gold is closing above $4,000.00, while silver bulls aim to close prices above $50.00. Source

Aakash Doshi, Head of Gold Strategy at State Street Investment Management, maintains a bullish outlook for gold, arguing that the metal is still underowned despite an unprecedented rally that saw its best quarterly gain in over 40 years. Gold's price surge—up nearly 17% in the last three months and 47% year-to-date—is supported by significant investment demand, which peaked in September with record inflows into the world's largest gold-backed ETF, SPDR Gold Shares (GLD). However, Doshi notes that total ETF holdings remain below their 2020 peak, indicating that gold is not yet an overowned asset. He views the high price level as warranted and sustainable, reflecting investors' need to hedge and protect against current extraordinary market conditions, including structural factors and various risks.

Doshi asserts that gold reaching $4,000 an ounce is a matter of "when, not if," supported by a weakening US dollar due to the Federal Reserve's new easing cycle, which is causing a bull-steepening curve in the bond market. Furthermore, gold remains an attractive insurance policy against global economic uncertainty, even as falling rates boost equity markets to record valuations. Although recession risks are currently low, Doshi points out they are increasing, which will continue to support gold's safe-haven allure. He also suggests that a prolonged US government shutdown could have negative growth consequences, further boosting gold prices and increasing the risk of credit rating downgrades. While he expects the rally's pace to slow from September's extraordinary rate, he sees new support holding at $3,500 an ounce, expecting any dips to be bought. Source

Goldman Sachs Research, led by analyst Lina Thomas, projects that gold prices will climb an additional 6% to reach $4,000 per ounce by mid-2026. This updated forecast is driven by strong, structural demand from two key buyer groups. The first group, "conviction buyers," including central banks, exchange-traded funds (ETFs), and speculators, consistently purchase gold regardless of price, motivated by hedging and economic views; their thesis-driven flows are the primary price setters. The research indicates that every 100 tonnes of net purchases by these conviction holders typically results in a 1.7% rise in the gold price. The second group, "opportunistic buyers" like emerging market households, provide price support by entering the market when they perceive the price as favorable.

The primary driver for this bullish outlook is the sustained buying from central banks, particularly those in emerging markets, whose accumulation pace has increased fivefold since 2022 following the freezing of Russia's foreign-currency reserves. Goldman Sachs views this as a structural shift in reserve management and expects the trend to continue for at least three more years as these central banks remain underweight gold compared to their developed market peers. This view is supported by a World Gold Council survey showing 95% of central banks expect global gold holdings to increase, and 43% plan to increase their own holdings—the highest level since 2018. Additionally, the forecast is bolstered by expected easing from the US Federal Reserve, which supports ETF demand, and a significantly bullish speculative positioning in the COMEX derivatives market. Goldman Sachs also recommends gold as a crucial commodity for diversifying portfolios against risks like high global policy uncertainty and supply shocks, as it has historically delivered positive performance when both stocks and bonds offered negative real returns. Source

The US government's premier measure of employment, the nonfarm payrolls report from the Bureau of Labor Statistics (BLS), is being widely criticized by economists and market analysts as antiquated, inaccurate, and misleading, especially given the current government shutdown. Kevin Grady, president of Phoenix Futures and Options, argues that the data is collected using "1970s metrics" and that its voluntary survey participation rate has dropped significantly to 40%, making it less representative. Compounding the issue are massive, delayed revisions, such as the preliminary subtraction of 911,000 jobs—the worst on record—which market participants like Grady argue prove the data is flawed. Grady contends that if the Federal Reserve (Fed) had the correct, timely data, it would have cut rates sooner, underscoring the severe real-world impacts of inaccurate reporting on mortgage rates, credit card interest, and even the US debt burden.

Meanwhile, Adam Button, head of currency strategy at Forexlive.com, believes the key issue that has rendered the report all but useless is the recent shift in immigration policies, which has led to the US subtracting people from the labor force for the first time in decades. This unprecedented demographic change means that a low-growth headline nonfarm payrolls number is no longer a reliable indicator of the jobs market's health, as the unemployment rate may remain low regardless. Button warns that most models used by the Fed and the private sector are outdated and cannot account for this mass net migration out of the United States. Consequently, policymakers and traders are being misled, creating a "really difficult period" where negligible job growth may pressure the Fed to cut rates based on an illusion, and investors must be cautious, potentially focusing on the unemployment rate instead of the volatile headline jobs number. Source

Image Source: Kitco News

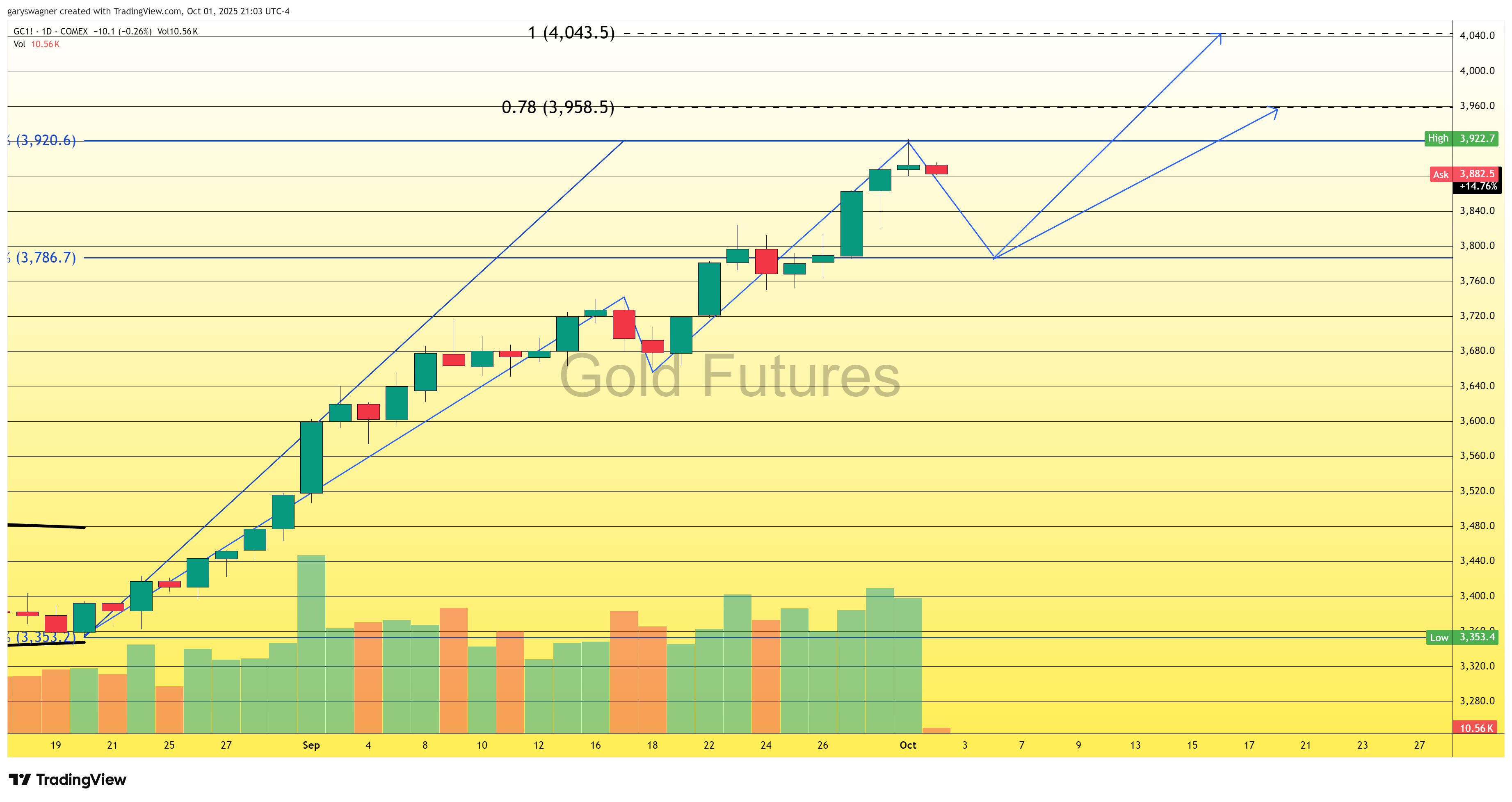

Gold prices settled modestly higher during today's session, achieving an intraday record high of $3,922.70 for the December futures contract. This surge was initially driven by two primary factors: intensified safe-haven demand stemming from the US government's impending shutdown and a severely disappointing ADP employment report, which revealed US firms eliminated 32,000 jobs in September. This weak hiring data, marking the second consecutive month of private employment contraction, reinforced market expectations that the Federal Reserve will continue its rate reduction cycle. Lower interest rates fundamentally support gold by decreasing the opportunity cost of holding the non-yielding asset.

Despite favorable fundamental conditions, including the neutral dollar and reinforced easing expectations, a puzzling price dynamic emerged: gold retreated substantially from its record intraday high to settle at $3,892.60. This price action formed a "shooting star" candlestick pattern, which technical analysts view as a potential bearish reversal signal that gains significance following a strong uptrend. For this signal to be confirmed, analysts are looking for a bearish candle in the following session that closes below today's levels, or for a surge in trading volume accompanying the shooting star, which would indicate a broad rejection of higher prices. The coming sessions will determine whether this technical signal marks a brief pause or a meaningful inflection point in gold's historic ascent. Source

Disclaimer: These articles are provided for informational purposes only. They are not offered or intended to be used as legal, tax, investment, financial, or any other advice.

Featured Image - Source: Unsplash