x

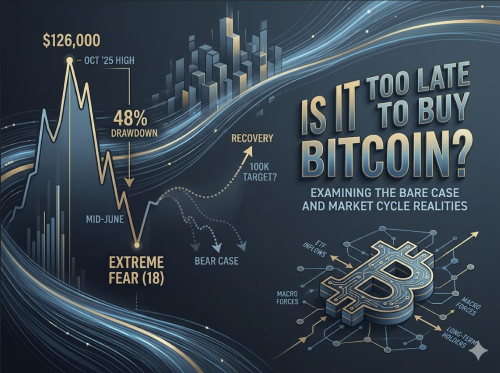

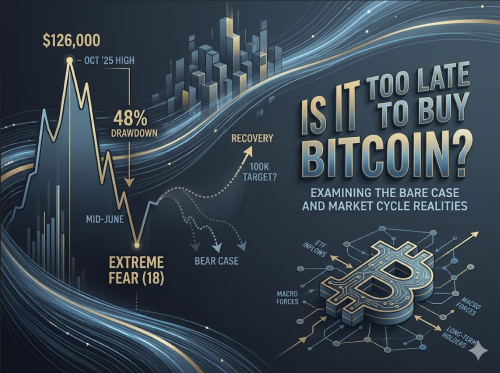

The cryptocurrency market is experiencing a profound sense of anxiety. Bitcoin has suffered a substantial correction, dropping nearly fifty per cent from its previous peak of one hundred and twenty-six thousand dollars down to the sixty-five thousand dollar mark. Investor sentiment has plummeted deeply into extreme fear, major spot Bitcoin exchange-traded funds (ETFs) have witnessed record-breaking outflow streaks, and corporate giants have made headlines by executing their first asset sales in years.

For many observers, it feels as though the definitive top is in and the party is over. However, this precise scenario raises a historical question that has echoed through every single cryptocurrency market cycle: Is it too late to buy Bitcoin?

This sense of missing the boat is not a novel feature of the current market; it is a recurring psychological milestone. Looking back to the historic market run of 2013, when Bitcoin climbed from thirteen dollars to over eleven hundred dollars, early community members openly lamented that they had missed the peak when the asset first hit one hundred dollars. The infrastructure back then was notoriously complex, and many individuals simply gave up attempting to navigate early exchanges.

A similar narrative played out in early 2017 when Bitcoin clawed back to one thousand dollars. Mainstream financial commentators dismissed the asset as a speculative bubble akin to historical tulip mania. Yet, within twelve months, the price rocketed to nearly twenty thousand dollars. When the market subsequently collapsed by over eighty per cent during the 2018 bare market, countless obituaries were written for cryptocurrency. Remarkably, an investor who bought at the absolute worst moment of that 2017 peak would still be up by hundreds of per cent today.

The pattern repeated yet again during the 2021 cycle, which peaked at sixty-nine thousand dollars, only to drop back down to fifteen thousand five hundred dollars following high-profile industry collapses. From that devastating bottom, the asset rallied by over seven hundred per cent to its 2025 high. Historically, the urgent question of whether it is too late has not been a signal of the final top, but rather an indicator of maximum cyclical fear.

While the current market feels remarkably painful, an objective analysis of the data reveals a critical structural difference between this draw-down and prior cycles. At roughly forty-eight per cent, this is the shallowest post-peak correction in the asset's history. Previous major bare markets saw devastating plunges ranging between seventy-eight and eighty-four per cent.

Market analysts point to two primary reasons for this newfound stability. Firstly, the introduction of spot Bitcoin ETFs has established a structural floor of institutional, long-term allocators that simply did not exist in earlier decades. Secondly, the root cause of this sell-off is macroeconomic rather than systemic. In previous cycles, the floor fell out because major crypto exchanges and lending platforms blew up. This time around, there are no widespread systemic collapses within the industry. Instead, external macro factors—specifically rising Treasury yields and a hawkish Federal Reserve pulling capital out of risk assets—are driving the price action.

Data indicates that long-term conviction remains incredibly robust. Over sixty per cent of the circulating supply has not moved in over a year. The core base of long-term holders is choosing to sit tight, refusing to flinch despite the broader market turbulence.

To navigate the market objectively, one must honestly evaluate the arguments presented by market bears. The recent negative data points are substantial and deserve careful consideration:

When examined through the lens of market history, these bearish points lose some of their catastrophic weight. Regarding the ETF outflows, senior industry analysts note that the billions lost represent a tiny fraction of the total assets under management, making the movement relatively minor in the grand scheme of institutional adoption. Furthermore, recent data shows that this selling pressure has already begun to exhaust itself, with net inflows quietly resuming. The smart money interpretation is that this was largely a leverage-driven cohort exiting positions, rather than long-term institutional allocators abandoning the asset.

Similarly, the widely reported corporate sales represent a mere rounding error. In one instance, an institution sold a tiny fraction of a per cent of its total holdings for corporate maintenance, only to turn around and purchase a significantly larger amount of asset volume shortly after.

Ultimately, price projections of forty thousand dollars remain hypothetical. While the market could certainly grind sideways or experience further liquidations, competing institutional models argue that the recent local lows represent the actual cyclical bottom, setting up a path toward a six-figure valuation by the end of the year.

The hesitation to participate in the market usually stems from a fixation on entering at the perfect price. However, extensive historical data from traditional finance indicates that investor behaviour matters far more than precise market timing.

Studies consistently show that the average investor drastically underperforms the broader market indexes simply by buying high during periods of euphoria and selling low during periods of panic. Mistimed withdrawals right before major market rallies severely damage long-term returns. Missing just a handful of the best trading days over a multi-year period can cut total investment returns in half. Crucially, the best market days almost always cluster immediately after the worst, most terrifying days.

Further research confirms that an investor who systematically allocates capital at the absolute worst market peak every year still vastly outperforms an individual who chooses to sit entirely in cash. In short, being active in the market with poor timing historically beats sitting on the sidelines out of fear.

Instead of obsessing over whether the price is too high or too low, market participants generally achieve better clarity by focusing on three structural principles:

Ultimately, the anxiety of being "too late" is rarely about the mathematical price on the screen. Too late almost always translates to being too scared. While there are no guarantees and the market may well experience further downward pressure before a true recovery, history suggests that the moments of deepest market fear are precisely where the long-term questions resolve themselves.

Coin Bureau - Is It Too Late to Buy Bitcoin?

"Bitcoin has crashed nearly 50% from its 2025 high. Does that mean it’s all over, or are we staring at yet another massive opportunity? Find out what really happens to those who buy when fear is at its peak, with charts, bear calls, and bull-proof numbers covering every “too late” panic in Bitcoin’s history.

We walk through the ETF moves, on-chain signals, price data, and why drawdowns like this one keep repeating. See what sets 2026’s correction apart and the real numbers most investors miss. Watch this before you decide to buy or bail—this cycle isn’t playing out like the last."

~ TIMESTAMPS ~

0:00 – Bitcoin Crashes 50%: Is The Bull Market Over?

1:56 – Every Time Investors Thought They Were Too Late

4:31 – Why This Bitcoin Crash Is Different From 2018 & 2022

6:05 – The Bear Case: Could Bitcoin Fall To $40K?

7:47 – Why The ETF Panic May Be Completely Overblown

9:28 – The Biggest Investing Mistake Almost Everyone Makes

11:03 – DCA vs Lump Sum: Which Wins During A Crash?

13:14 – Is $65K A Generational Buying Opportunity Or A Trap?

Source 👉 https://www.youtube.com/watch?v=8j3DotIC0ss

Disclaimer: This article is provided for informational purposes only, mistakes may be made, and it's not offered or intended to be used as legal, tax, investment, financial, or any other advice.