x

By Tim Hakki

Bitcoin and Ethereum. Image: Shutterstock

This week in coins. Illustration by Mitchell Preffer for Decrypt.

The prices of crypto market leaders Bitcoin and Ethereum typically move together. But some weeks form an exception, and this was just such a week.

(10).png)

Bitcoin, the No. 1 cryptocurrency in the world with a $380 billion market cap, fell another 2% over the past week and trades for around $19,860 on CoinMarketCap at the time of writing on Saturday morning.

Ethereum, the No. 2 crypto asset with a market cap of $190 billion, rose a modest 3.5% over the past week and currently trades at $1,556.

New data this week from the Ethereum Name Service (ENS) tells a more bullish story. ENS was launched five years ago by members of the Ethereum foundation to enable people to register memorable domains for their crypto wallets, instead of being limited to the unwieldy string of random numbers and letters that typically represents a blockchain address.

ENS reported its third highest month of revenue over August, with 2.17 million .ENS domain names created on the service. A fortnight ago, the service reported that over the preceding three months, the number of registrations for .ENS domain names had doubled.

This dramatic spike in ENS activity is likely in anticipation of Ethereum’s major network overhaul coming this month. The Ethereum merge will transition the network from the energy-intensive proof-of-work (PoW) consensus mechanism to the 99.95% greener proof-of-stake (PoS) algorithm.

The biggest loser among the top thirty cryptocurrencies was Avalanche. AVAX sank 10% over the week; it’s worth under $20 this Saturday.

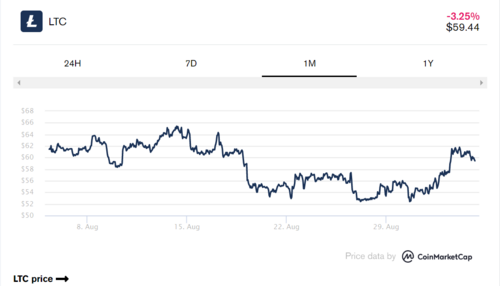

Two cryptocurrencies in the top 20 enjoyed big rallies, and one of them may come as a surprise to many: Litecoin (LTC) blew up 15% in the past week to over $60, while Polygon’s MATIC surged 11% and currently trades for around $0.90. Polygon’s blistering rally came amid adoption news from trading app Robinhood and social media giant Meta.

The other leading cryptocurrencies barely moved this week.

On Monday, the managing director of Singapore’s Monetary Authority (MAS), the country’s central bank and financial watchdog, Ravi Menon, said at a Green Shoots fintech seminar that the regulator will begin adding hoops to jump through for retail investors who want to get into crypto. The proposals include customer suitability tests and limiting access to credit facilities.

Menon said the measures are to protect consumers, elaborating that while Singapore welcomes fintech innovation, investors “seem to be irrationally oblivious about the risks of cryptocurrency trading,” but an outright ban “is not likely to work.” The MAS is also looking to bring in international regulatory reviews and collaborate on harm reduction measures.

.gif)

Paraguayan leaders also spoke about regulation on Monday. President Mario Abdo Benítez vetoed a bill that would have regulated various crypto activities in the country, including mining. According to the Executive decree, the primary reason for the veto was that energy costs would allegedly outweigh the employment benefits.

In the U.S., Rep. Raja Krishnamoorthi—Chair of the Subcommittee on Economic and Consumer Policy, a part of the House, which forms Congress along with the Senate—sent letters to five of the largest crypto exchanges in the U.S. on Tuesday, requesting “information and documents” on how they’re working to “combat cryptocurrency-related fraud.”

Krishnamoorthi also mailed four federal agencies—the U.S. Department of Treasury, Securities and Exchange Commission, Commodity Futures Trading Commission, and Federal Trade Commission—to solicit policy suggestions and opinions on whether cryptocurrencies should be defined as “commodities, securities, or both.”

Facebook and Instagram parent company Meta rolled out new NFT features for its properties that day, including the ability to cross-post NFTs in-app for select U.S. users.

Meta currently supports Ethereum, Polygon, and Flow NFTs on both Facebook and Instagram. It also supports a number of crypto wallets, including MetaMask, Rainbow, Trust Wallet, Coinbase Wallet, and Dapper, which can all be connected to verify and share NFTs.

.png)

On Wednesday, ticketing titan Ticketmaster announced it will utilize Dapper Labs’ Flow blockchain to mint NFT tickets for certain events. In the last six months, Dapper Labs and Ticketmaster have quietly piloted an NFT program in which Ticketmaster issued ticket NFTs as memorabilia to attendees of specific events, like this year’s Super Bowl LVI.

More than five million Flow NFTs were minted during the pilot, according to Dapper.

Singapore-based crypto lender Hodlnaut was granted judicial management to organize and restructure by the country’s High Courts on Tuesday. The firm filed for judicial management on August 13 seeking temporary protection from legal claims. Just five days prior, it had frozen customer withdrawals to “stabilize liquidity” during the industry’s ongoing liquidity crisis.

On Thursday, bankrupt crypto lender Celsius said in a court filing that it is seeking to return some of its customers’ funds. The company is currently offering to release nearly $50 million in crypto belonging to customers who were a part of the “custody” program—accounts that stored crypto but did not generate returns.

If Celsius’s proposal is approved, the returned funds would only cover a fraction of the lender’s obligations: custody accounts make up $210.02 million in crypto, according to the filing. However, customers expecting returns who invested crypto in Celsius’s popular “earn” program account for $4.3 billion in assets; there was no word on when they’ll get their money back.

Bitcoin is getting harder to mine. According to data from BTC.com, Bitcoin’s mining difficulty jumped 9.26% over the last two weeks. As difficulty increases, miners may face slimmer profits, since more computing power (and energy) is needed to mine while the value of Bitcoin has remained stagnant.

Scott Norris, co-founder of private Bitcoin miner LSJ Ops, told Decrypt that “difficulty shrinking is the cause for concern,” because it would mean more miners are dropping off the network—making it less efficient.

Norris added: “A difficulty increase is an indicator of a strong and growing network, it's actually a good thing,” he said, adding that “sectors like gas and hydro are championing cheap energy costs and allowing for a new generation of long term mining to emerge.”

.png)